- Insights

- Featured Insights

As a long-term member of the Financial Action Task Force (FATF), Australia’s anti-money laundering and combatting the financing of terrorism (AML/CFT) regulatory framework seeks to align with the recommendations laid out by the agency.

These recommendations require governments to:

- Criminalize money laundering and terrorist financing activities;

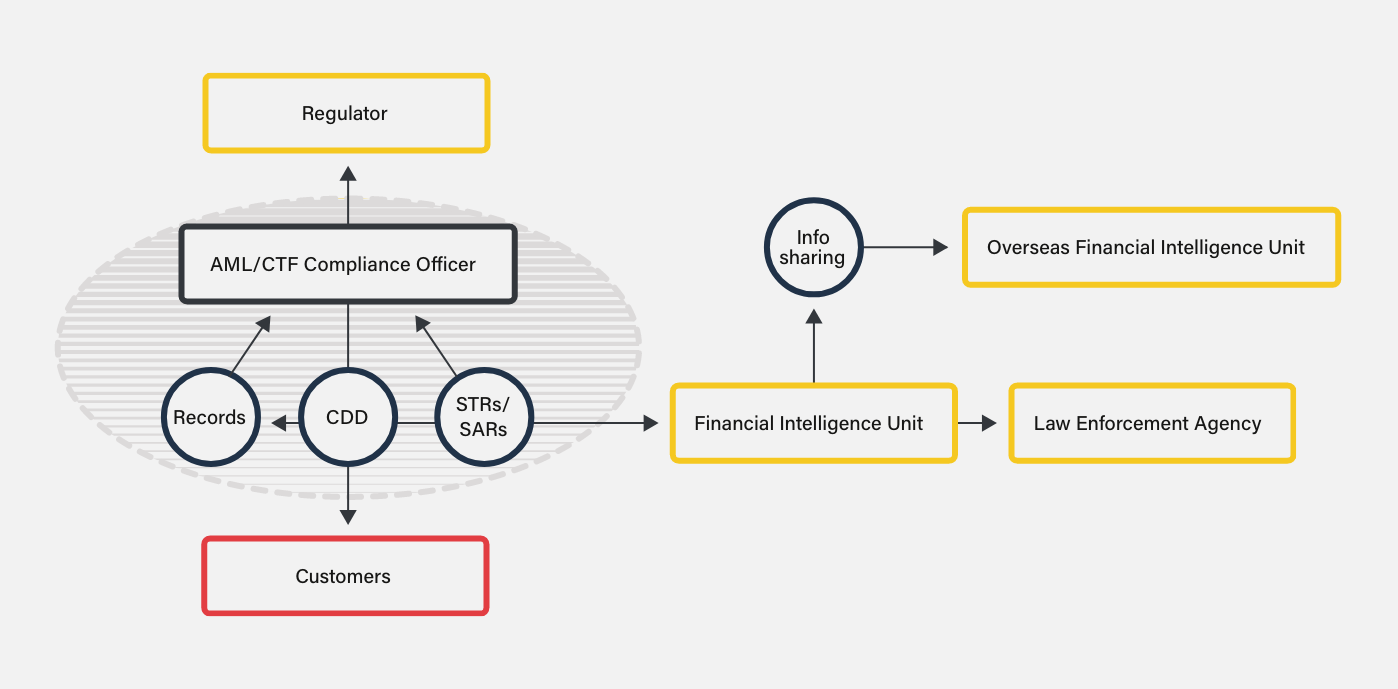

- Obligate key elements of the private sector to act as watchdogs over the activities of their customers through Customer Due Diligence (CDD), record keeping, and the reporting of suspicious activity, subject to tipping off and confidentiality protections;

- Create or task an existing government agency – a “Financial Intelligence Unit” (FIU), to receive and action private sector reporting; and

- Create or task an existing regulator/supervisor (or more) to ensure that the private sector fulfills its obligations and launch appropriate enforcement action if not.

Commonly, this creates an AML/CTF ecosystem shown in a simplified form in the diagram below.

Australia’s AML regulations were initially implemented as a direct response to two Royal Commissions that exposed the relationship between money laundering, fraud, major tax evasion, and organized crime in the 1980s. The Costigan and Stewart Royal Commissions identified the need for legislative strategies to address these growing issues, which led to Australia’s primary AML legislation, the Financial Transaction Reports Act 1988 (FTR Act).

Australia’s FTR Act now operates alongside the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 (AML/CTF Act), establishing the country’s compliance framework alongside:

- The AML/CTF Rules Instrument 2007, which provides details about implementing the Act for the private sector

- The AML/CTF (Prescribed Foreign Countries) Regulations 2018, which outline specific regulations related to North Korea and Iran

However, in light of the FATF’s Mutual Evaluation Report (MER) of Australia in April 2015, the country’s AML/CFT framework is currently undergoing a long-term overhaul. According to the MER, Australia’s approach:

- Lacked sufficient CDD requirements

- Contained problems with correspondent banking controls

- Failed to include designated non-financial businesses and professions (DNFBPs) as designated entities.

As part of the reform process, a statutory review by the Australian Attorney General made various recommendations, which have subsequently become known as “Tranche 1.5” and “Tranche 2.” The AML/CTF and Other Legislation Amendment Act 2020 and the AML/CTF Increased Transparency Bill have also been proposed to provide more scope for information sharing around suspicious activity and between the public and private sectors and introduce a Beneficial Ownership (BO) registry.

A Guide to AML for Australian FinTechs

Uncover the core compliance responsibilities that arise from Australia’s AML/CTF regime and how FinTechs should respond using a risk-based approach.

Download the guideOriginally published 15 September 2022, updated 01 July 2026

Disclaimer: This is for general information only. The information presented does not constitute legal advice. ComplyAdvantage accepts no responsibility for any information contained herein and disclaims and excludes any liability in respect of the contents or for action taken based on this information.

Copyright © 2026 IVXS UK Limited (trading as ComplyAdvantage).