- Insights

- Featured Insights

The US regulatory landscape in 2026 is defined by a striking paradox: while the federal government has dramatically scaled back reporting requirements for domestic small businesses, it has simultaneously tightened the noose on foreign entities, digital asset issuers, and the “black box” of artificial intelligence. For compliance teams, the standard playbook is being rewritten in real-time.

Drawing on key insights from our State of Financial Crime 2026 report, this blog outlines the top four trends shaping the new compliance reality for US financial institutions (FIs) in 2026.

1. Narrowing beneficial ownership reporting requirements

On March 21, 2025, the Treasury Department’s Financial Crimes Enforcement Network (FinCEN) fundamentally reshaped the Corporate Transparency Act (CTA). Through an Interim Final Rule (IFR), the government drastically narrowed the scope of beneficial ownership information (BOI) reporting, effectively exempting nearly all domestic businesses and US citizens. This shift remains the governing framework for the 2026 compliance year.

The CTA’s enforcement now focuses exclusively on foreign reporting companies – entities formed under the laws of a foreign country that have registered to do business in the United States. This change collapsed the pool of reporting entities from an initial estimate of 32.6 million to approximately 20,000 (roughly 0.6% of the original target).

For compliance officers, the focus has shifted from high-volume data collection to high-precision verification of cross-border structures. Because domestic entities are now expressly exempt, FIs must ensure their onboarding workflows distinguish between a standard US LLC and a foreign entity registered to do business in the US, as only the latter carries a federal BOI filing obligation.

- 30-day filing window: Foreign reporting companies must file their initial BOI reports within 30 days of their US registration becoming effective.

- Domestic exemption: FinCEN guidance confirms that corporations, LLCs, and similar entities created by filing with a US Secretary of State are now exempt from federal BOI reporting.

- US person carve-out: Foreign reporting companies are not required to disclose “US persons” (citizens or residents) as beneficial owners.

- Individual immunity: US citizens are no longer required to provide their personal BOI to any reporting company, even if they hold a significant ownership stake in a foreign entity.

- Amnesty on prior penalties: The Treasury Department has confirmed it will not enforce civil or criminal penalties for failures to comply with the original (pre-2025) domestic reporting rules.

Legal note for 2026: While the IFR is currently in effect, the 11th Circuit Court of Appeals upheld the constitutionality of the underlying Act in late 2025. This solidifies the government’s authority to maintain the current “foreign-only” reporting structure as FinCEN moves toward a Permanent Final Rule.

2. Escalating sanctions enforcement

In contrast to the US’s deregulatory agenda, 2026 is marked by an escalation in sanctions enforcement, driven by the administration’s view of the fentanyl crisis as a threat to national security. Under Executive Order 14157, major drug cartels across Latin America and the Caribbean – including Mexico’s Sinaloa Cartel and Cartel de Jalisco Nueva Generación (CJNG) – have been designated as Foreign Terrorist Organizations (FTOs) and Specially Designated Global Terrorists (SDGTs).

For firms, this reclassification creates a new, sharper form of liability. The legal threshold has moved from “knowingly facilitating” to the stricter “material support” standard used in counter-terrorism law. This change means that even unintentional provision of funds, transport, or administrative services to these groups can now trigger felony charges.

This extends beyond financial institutions to include designated non-financial businesses and professions (DNFBPs), such as real estate brokers and accountants. The message for organizations is clear: while BOI reporting burdens have eased, the consequences of facilitating payments linked to designated entities have been elevated from a compliance failure to the risk of abetting a terrorist act.

3. Operationalizing stablecoin standards and reserve oversight

The transition into 2026 has brought a definitive shift in digital asset oversight following the enactment of the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act on July 18, 2025. This framework, a pillar of Executive Order 14178, has moved into active rulemaking. In February 2026, the Office of the Comptroller of the Currency (OCC) issued a formal proposal to establish capital standards and liquidity requirements for Permitted Payment Stablecoin Issuers (PPSIs). These 2026 rules introduce two critical mandates that have reshaped the market:

- Prohibition on yield: PPSIs are strictly prohibited from paying interest or yield to holders, ending the “earn” programs that previously characterized the sector.

- Strict capital ratios: Issuers must maintain a one-to-one capital ratio in highly liquid reserves, with the OCC now projecting the stablecoin market to reach $500 billion by the end of the year.

Parallel to this, the US has solidified its role as a major holder of digital assets. Established on March 6, 2025, the Strategic Bitcoin Reserve and the United States Digital Asset Stockpile are now permanent fixtures of national fiscal policy. As of March 2026, the federal government is estimated to hold approximately 328,000 BTC. This includes the landmark $15 billion seizure linked to the Prince Group’s forced-labor scams, which resulted in the convictions of three directors in early 2026. Heading further into 2026, the Treasury is leveraging a March 2026 report to Congress to prioritize AI-driven detection of illicit activity, pushing regulated institutions to integrate advanced blockchain monitoring and digital identity verification to manage the financial stability and illicit finance risks inherent in this new digital era.

4. Navigating regulatory patchwork

In the United States, the regulatory landscape for AI in financial services has reached a critical inflection point, characterized by a complex “patchwork” of state-level mandates and federal preemption efforts. While states like Colorado have moved to enforce rigorous “algorithmic discrimination” audits for all high-risk financial systems starting June 30, 2026 (Colorado SB24-205), and California has implemented mandatory training-data transparency as of January 1, 2026 (California AB 2013), the federal government has countered with a push for national uniformity. Key to this shift is the Treasury’s March 2026 Financial Services AI Risk Management Framework (FS AI RMF), which provides a granular 230-point matrix to move firms from “black box” experimentation to defensible compliance. Simultaneously, the Department of Justice’s AI Litigation Task Force is actively challenging “onerous” state laws to prevent a fragmented regulatory environment that could stifle innovation in AML and fraud detection. Consequently, financial institutions are caught between maintaining state-specific protections and adopting a standardized federal “risk-based” approach.

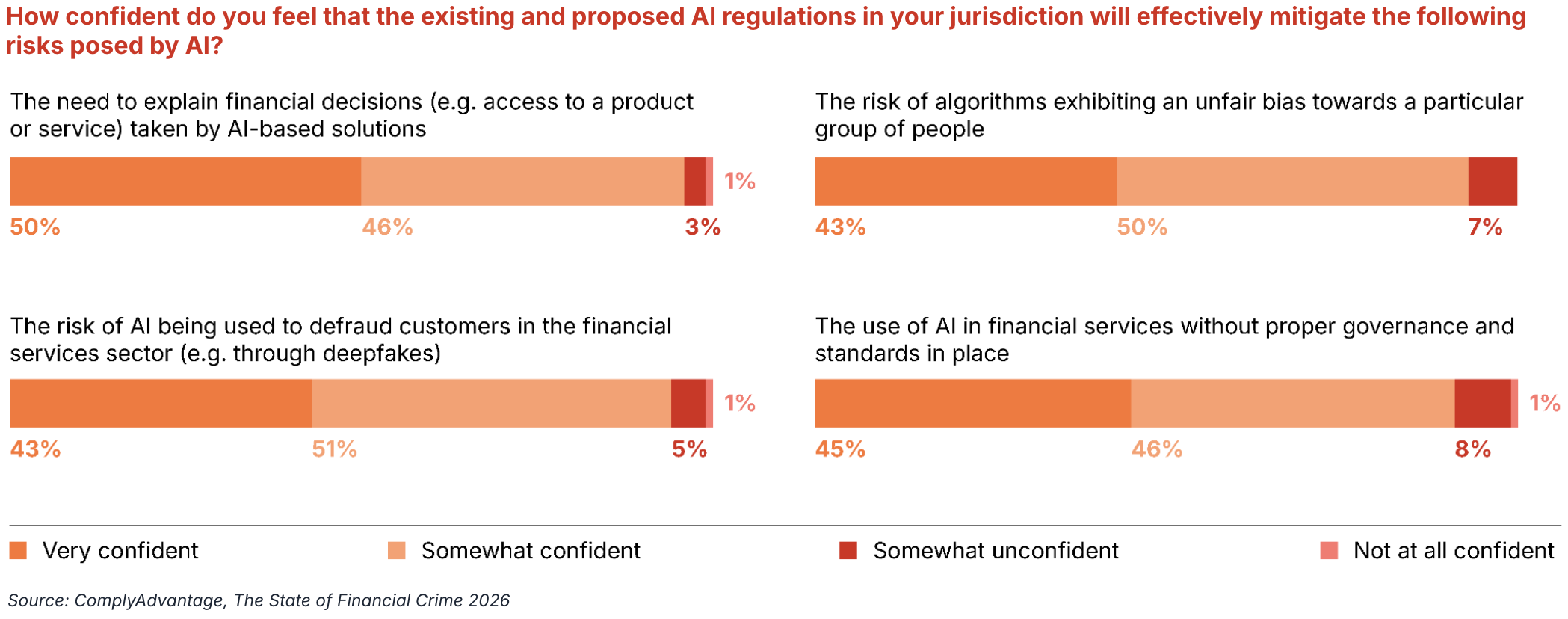

Against this patchwork of emerging AI regulation, firms are actively evaluating their readiness and the effectiveness of legislative efforts in mitigating core risks. When asked, “How confident do you feel that the existing and proposed AI regulations in your jurisdiction will effectively mitigate the following risks posed by AI?”, our 600 respondents expressed high confidence that existing and proposed AI regulations will effectively mitigate key risks:

- Risk of AI being used to defraud customers: 94% (43% very confident, 51% somewhat confident) were confident that regulation will address the risk of AI being used to defraud customers (e.g., through deepfakes).

- Need to explain financial decisions: 96% (50% very confident, 46% somewhat confident) were confident in regulations mitigating the need to explain financial decisions taken by AI-based solutions.

- Use of AI without proper governance: 92% (46% very confident, 46% somewhat confident) were confident in regulations addressing the use of AI in financial services without proper governance and standards in place.

- Risk of unfair bias: 93% (43% very confident, 50% somewhat confident) were confident that regulation will address the risk of algorithms exhibiting an unfair bias towards a particular group of people.

Furthermore, when asked, “Does your organization have an assurance program for AI to ensure its effectiveness, auditability, and adherence to privacy standards & model risk governance?”, 98% of organizations stated they had a program in place or had started establishing one. The data shows that while commitment is high, implementation lags: our survey reveals that 42% of organizations have yet to fully establish or create a comprehensive AI assurance program. This means that while firms feel legislatively confident, a significant portion of the industry is still working to build the full governance and auditing structures needed to defend automated decisions and mitigate algorithmic bias.

However, despite the overwhelming confidence (94%) that regulations can mitigate AI-enabled fraud, the sheer pace of generative AI development raises a crucial question: Will current regulatory frameworks and proposed legislation be agile enough to keep pace with the evolving capabilities of large language models and other generative AI tools used in fraud and money laundering?

The State of Financial Crime 2026

Get insights on financial crime trends from our global survey of 600 senior decision-makers and expert guidance from our Financial Crime Compliance Strategy team.

Download nowOriginally published 19 March 2026, updated 19 March 2026

Disclaimer: This is for general information only. The information presented does not constitute legal advice. ComplyAdvantage accepts no responsibility for any information contained herein and disclaims and excludes any liability in respect of the contents or for action taken based on this information.

Copyright © 2026 IVXS UK Limited (trading as ComplyAdvantage).