- Insights

- Featured Insights

The Autorité des Marchés Financiers (AMF) is an independent French regulator responsible for safeguarding and monitoring France’s financial market, its participants, and their investments in its financial services. Within the framework of anti-money laundering and countering the financing of terrorism (AML/CFT), the AMF investigates and sanctions regulatory breaches. The Financial Security Act (2003) established the AMF as the independent regulatory body responsible for supervising France’s financial markets. The creation of the AMF represented a merger of three French financial oversight bodies: the Commission des Opérations de Bourse (COB), the Conseil des Marchés Financiers (CMF), and the Conseil de Discipline de la Gestion Financière (CDGF). Headed between 2017 and 2022 by Robert Ophèle, the AMF is funded by fees collected from the financial institutions it supervises.

The AMF conducts AML/CFT activities under Article L. 561-36 of the French Monetary and Financial Code. It uses its authority to ensure financial institutions operate per legislative policy and meet its anti-money laundering regulation compliance standards.

What does the AMF do?

The AMF has three objectives:

- To safeguard investments in financial products

- To ensure that investors receive sufficient information about financial products

- To maintain orderly financial markets

The AMF’s Jurisdiction

In its duty to French financial institutions, the Autorité des Marchés Financiers oversees all participants and products operating within the country, including:

- Asset management companies

- Financial advisors

- Crowdfunding advisors

- Central securities depositories

The AMF’s Powers and Responsibilities

To identify and prevent money laundering (ML), terrorist financing (TF), and other fraudulent activities, the AMF can:

- Set rules

- Conduct investigations

- Issue sanctions and fines to companies that breach compliance obligations

The AMF may also censure individuals within a financial institution, including:

- Company directors

- Employees

- Officers

- Anyone acting on behalf of a financial entity

In concrete terms, the AMF’s fight against money laundering is based on several key elements:

Risk-Based Vigilance

The Autorité des Marchés Financiers requires French financial institutions to maintain sufficient vigilance in updating their clients’ risk profiles. That obligation means that every financial institution must be able to perform risk classification procedures and implement its AML policies and control systems using AMF guidelines. The level of vigilance required by the financial institution should reflect the level of risk each client presents.

Reporting Obligations

The AMF also requires financial institutions to report any suspicious behavior relating to money laundering to the French authorities. Specifically, companies must report to Traitement du Renseignement et Action Contre les Circuits Financiers Clandestins (TRACFIN), the French Ministry of Finance’s enforcement body that the AMF works with to enforce its money laundering regulations.

Audits and Inspections

To enforce money laundering regulations and assure compliance, the AMF conducts audits and inspections of French financial institutions, focusing on internal AML procedures and infrastructure, and individuals in charge of AML compliance. Breaches in compliance are reported to the AMF Enforcement Committee.

Coordination with French Authorities

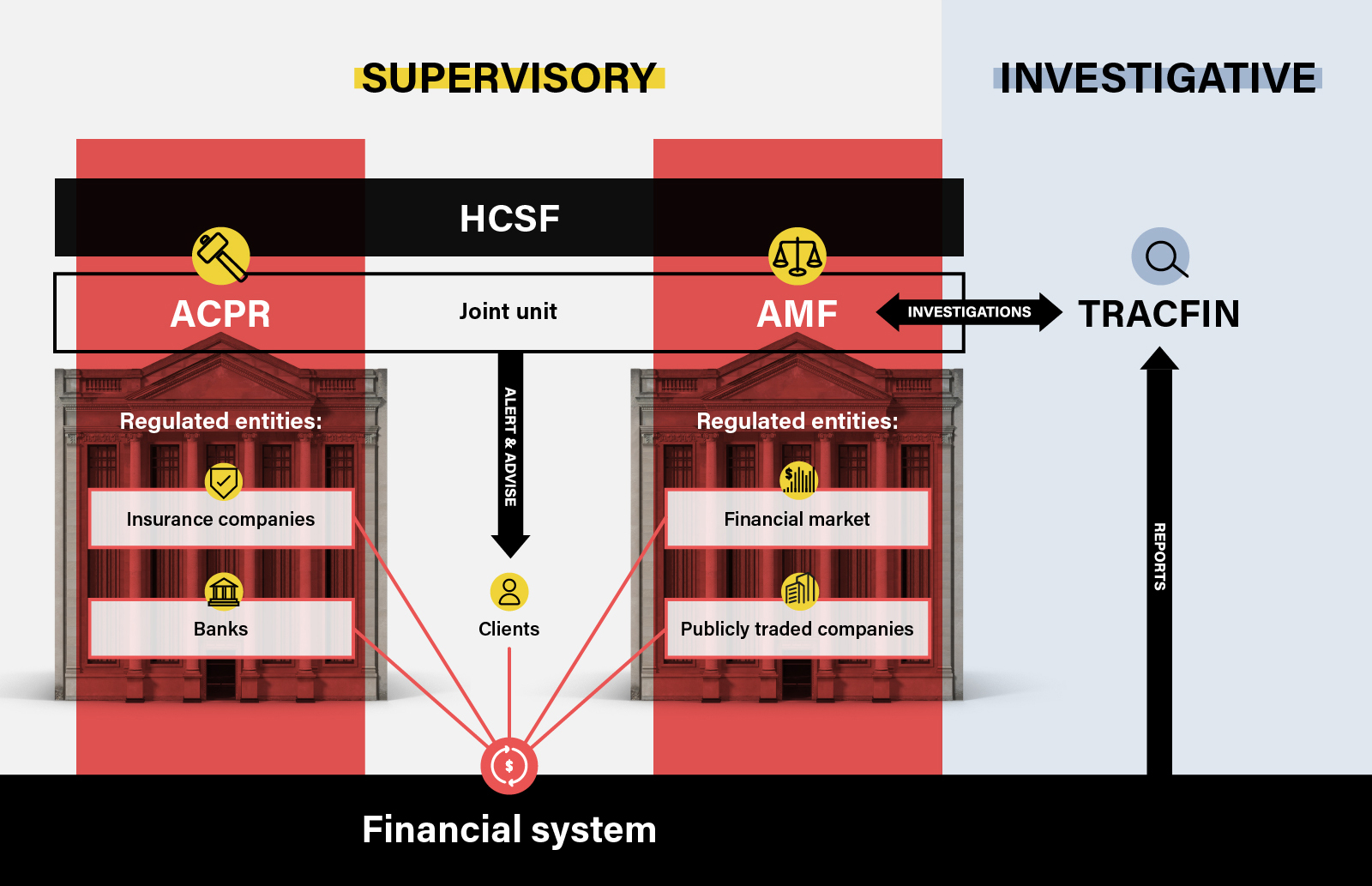

The AMF contributes to broader efforts in combating money laundering and ensures France’s national AML performance is held to the highest standard by collaborating with associated national bodies. In this capacity, the Autorité des Marchés Financiers works with the Autorité de Contrôle Prudentiel et de Résolution (ACPR) and TRACFIN to communicate AML/CFT risks to regulated professions.

AMF: Its Current Outlook

The FATF’s 2022 Mutual Evaluation Report on France highlighted several strengths and weaknesses and made corresponding recommendations. Regarding the AMF’s strengths, the FATF highlighted particular successes, including:

- Regular and effective cooperation with the ACPR and TRACFIN – Beyond facilitating these entities’ internal exchanges, their collaboration allows the AMF and ACPR to effectively communicate ML/TF risks to regulated institutions.

- Close AML/CFT cooperation with virtual asset service providers (VASPs) – The AMF requires these organizations to register with it and assists them in deploying risk-based AML/CFT programs.

- Risk-based supervision of financial institutions (FIs) – In the most critical sectors, the AMF performs on-site inspections appropriately. It also has an excellent overall understanding of France’s national ML/TF risks.

Nevertheless, the FATF also identified several areas for improvement:

- Cumbersome, ineffective disciplinary sanctions for non-compliant firms – The agency has imposed only one sanction since 2016. To improve sanctions’ effectiveness, FATF recommended a shortened time between on-site inspections and the imposition of sanctions.

- A limited notion of “effective managers” of asset management companies (AMCs) – Although the AMF verifies new AMC managers and requires disclosure of appointments to certain vital functions – notably heads of management and compliance – its definition remains too narrow. The FATF notes that the regulator doesn’t include all management functions and does not monitor current managers on an ongoing basis.

- Insufficient risk-based supervision for specific sectors – AML/CFT controls remain inadequate for designated non-financial businesses and professions (DNFBPs), particularly real estate agents and notaries involved in this sector. However, the AMF only formalized its risk-based supervision over the financial market in 2020. Therefore, it will still take time to assess it thoroughly.

AMF, TRACFIN, and ACPR: How Do They Collaborate?

The AMF and the ACPR are part of the High Council for Financial Stability (HCFS), a regulatory body that seeks to safeguard the financial system against destabilization – such as the 2008 financial crisis. As such, these entities work together even though they oversee different financial sectors. While the AMF oversees the financial markets sector, the ACPR oversees the insurance and banking sectors.

In 2010, these two bodies established the AMF and ACPR Joint Unit, which publishes an annual report on capital market commercial practices and provides valuable information to better protect customers in the banking, insurance, and financial services sectors. In addition, the AMF and ACPR regularly issue warnings about the unauthorized foreign exchange market (Forex) to protect investors. In 2022, they organized the 3rd edition of the AMF/ACPR Fintech Forum, which took place on October 19. According to the AMF, this forum seeks to bring together players in innovative finance, discussing the sector’s major regulatory issues.

While the AMF and the ACPR regulate and intervene in the French financial system, TRACFIN analyzes suspicious transaction reports (SARs) submitted by regulated organizations, conducts investigations, and communicates its observations to competent authorities. TRACFIN is essential to AML/CFT efforts and collaborates with the AMF and the ACPR to this end. In 2021, the AMF and TRACFIN published joint guidelines to explain TRACFIN reporting obligations to regulated professions. Similarly, the AMF regularly collaborates with TRACFIN on investigations. In 2022, the two organizations unveiled a new cooperation protocol, the previous version of which dates back to 2012.

Discover how to optimize your AML/CFT programs in light of the EU’s new regulations

A Guide to the European Union’s New AML/CFT Framework

Originally published 22 May 2019, updated 14 December 2022

Disclaimer: This is for general information only. The information presented does not constitute legal advice. ComplyAdvantage accepts no responsibility for any information contained herein and disclaims and excludes any liability in respect of the contents or for action taken based on this information.

Copyright © 2026 IVXS UK Limited (trading as ComplyAdvantage).