- Insights

- Featured Insights

The arrival of instant payment schemes like SEPA Instant Credit Transfers and services such as FedNow has reshaped the payments landscape. In the EU alone, real-time payment transactions are projected to reach 34.2 billion by 2027, up from 13.2 billion in 2022. As payment rails get faster and regulators get more specific about sanctions enforcement, picking the right payment screening software is a higher-stakes decision than it used to be.

Financial institutions (FIs) have a wide range of specialist solutions to choose from. The challenge is no longer finding options; it is selecting the one that fits the firm’s risk profile, its payment rails, and its operational model.

This article walks through the nine most important factors firms should weigh when making that choice.

What is payment screening software?

Payment screening software is the specialist technology that intercepts transactions at the point of execution and checks the parties to a payment against global sanctions lists, allowing firms to block or flag transactions that match. Although it is often grouped with broader anti-money laundering (AML) controls, payment screening is specifically a sanctions control. The question it answers is binary: is anyone in this transaction connected to a sanctions target?

The software checks information across multiple fields in a payment message, including sender, receiver, intermediary banks, BIC codes, and reference text, against sanctions sources such as the OFAC SDN list, the UK Sanctions List, the EU Consolidated List, and the UN Consolidated List. Firms can also screen against their own custom lists where they hold internal intelligence about high-risk counterparties.

Recent regulation has narrowed where transaction-level screening actually applies. Under the EU Instant Payments Regulation (IPR), payment service providers (PSPs) are prohibited from conducting transaction-level sanctions screening on in-scope SEPA Instant transfers, and must instead screen their customer base against EU sanctions lists at least daily. Cross-border payments, non-SEPA-Instant rails, and most domestic rails outside the EU continue to require transaction-level screening, which is where payment screening software earns its keep. Firms operating across multiple rails typically need both transaction-level screening and customer-level screening to cover all their obligations.

Why is payment screening important?

Payment screening is the interception layer that prevents firms from facilitating payments to or from sanctioned parties. It works alongside other compliance controls including customer screening, ongoing monitoring, and transaction monitoring, which together cover money laundering, terrorist financing, and other financial crime risks. PSPs across most jurisdictions are subject to AML/CFT regulations that require effective controls across this full stack.

When payment screening fails, the consequences are direct. Sanctions breaches carry civil and criminal penalties, individual liability for compliance leaders in some jurisdictions, and the operational risk of losing correspondent banking relationships that the business relies on to clear payments. Reputational damage compounds all of this in a market where regulated counterparties increasingly scrutinize each other’s controls before doing business.

9 tips for choosing your payment screening software

1. Understand your business requirements

AML compliance is built around the risk-based approach: compliance programs look different because firms have different risk profiles. The same applies to payment screening and the software used to deliver it. Firms should assess each potential solution against the payment types they support, the corridors they operate in, the customers they serve, and the sanctions exposure that profile creates.

Firms will always have multiple interests to balance. Aside from compliance obligations, reputational, operational, and commercial considerations will also shape software choice. Customer experience, growth plans, and analyst workflow all matter.

2. Consider your regulatory obligations

Payment screening sits at the intersection of two regulatory regimes: sanctions enforcement and payments infrastructure. Firms should understand both before choosing software.

On the sanctions side, the main enforcement bodies and lists firms screen against include OFAC and the SDN list in the US, OFSI and the UK Sanctions List in the UK, the EU Consolidated List enforced by member states, and the UN Security Council Consolidated List. National regimes for other jurisdictions also apply where relevant; Singapore, for example, primarily implements UN Security Council sanctions at the national level. Firms should check that their chosen software supports the lists relevant to their corridors and counterparties.

On the payments side, recent rules shape where and how transaction-level screening applies. In the EU, the IPR prohibits transaction-level sanctions screening on in-scope SEPA Instant transfers and instead requires daily customer-level screening. The EU Payment Services Regulation (PSR) and Third Payment Services Directive (PSD3), agreed in late 2025 and expected to enter into force in mid-2026 with a transition period before full application, will further tighten the operational requirements around all EU payments. In the UK, the Payment Services Regulations 2017 provide the operational framework for PSP obligations. The EU AI Act classifies AML and sanctions screening tools as high-risk, meaning automated screening decisions will need to be explainable when those obligations apply from August 2026.

Regulators will expect firms to be able to explain their choice of software and how it supports compliance with these obligations.

3. Select a solution that is accurate and efficient

Firms should understand the specific features of a payment screening solution and check it aligns with their needs. An effective solution draws on comprehensive, accurate, and current data, and screens reliably against that data to balance true positive detection with false positive reduction. Matching algorithms that account for variations in spelling and global naming conventions matter here, and firms should be able to adjust search parameters and fuzziness settings to focus screening on the data that is relevant to a given corridor or counterparty profile.

Sanctions lists change frequently, and a single missed designation can mean a breach. Firms should look for software that receives sanctions updates as close to real time as possible, ideally with critical lists refreshed in minutes through automated monitoring rather than manual cycles.

The Role of Technology and Talent in Transaction Screening

Based on expert advice and surveys of 600 industry leaders, our guide explains how firms can deliver faster and more effective transaction screening.

Download now4. Make sure the solution integrates with your existing systems

Siloed data and systems hinder compliance processes by limiting what analysts can see when responding to alerts. Payment screening software that integrates cleanly with the rest of a firm’s tech stack removes that barrier. Application programming interfaces (APIs), which let two systems exchange data and trigger workflows, are the most common integration approach. Pre-built integrations with common payment processing and case management systems also shorten the implementation timeline.

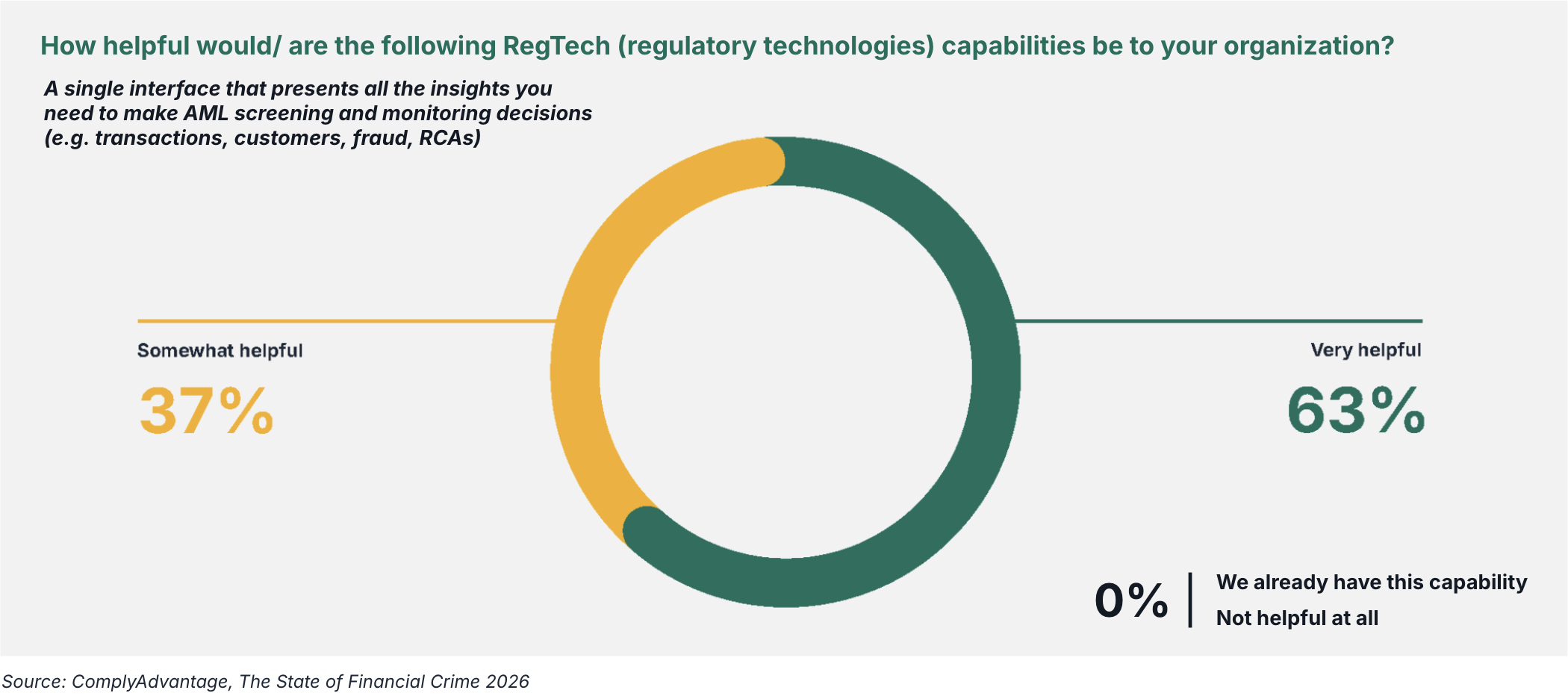

For many firms, integration is also a consolidation problem. According to our 2026 State of Financial Crime survey, 100% of the 600 firms surveyed said a single interface for AML solutions would be helpful, yet 53% still juggle between 8 and 10 different payment screening solutions. Choosing software that brings payment screening into the same workflow as customer screening and transaction monitoring reduces the number of systems analysts need to operate against and the volume of data hand-offs that go with them.

5. Test the solution’s usability

A payment screening solution that excels on paper but is difficult to operate in practice will not deliver value. Firms should check what implementation support is included, including documentation, FAQs, and access to ongoing vendor support. The availability of a sandbox, so firms can test risk models and screening configurations before going live, helps validate fit between the software and the team that will use it.

Specific features worth looking for include consolidated case views, automated event and customer risk scoring, alert prioritization, and accessible case documentation that supports a clear audit trail.

6. Make sure the solution covers data security and privacy needs

Compliance leaders should prioritize information security when assessing potential solutions, given the volume and sensitivity of the customer and transaction data involved in payment screening. Enterprise-wide risk assessments should include security and privacy, and firms should have strategies in place to resist cyber attacks and maintain business continuity if one occurs. Any payment screening software a firm adopts should align with those controls rather than add to the firm’s existing security surface. Firms should also be aware of their privacy obligations under regulations such as GDPR and confirm with vendors that their solutions can accommodate them.

7. Consider the cost-effectiveness of the solution

Budgets, timelines, and KPIs should all shape software choice. Larger firms making a significant investment should expect enterprise-grade compliance capabilities, including configuration flexibility, performance at scale, and depth of data, that lower-cost options typically do not deliver. For smaller firms with growth plans, scalability is the key consideration; a solution that fits today but cannot grow with the business creates an expensive re-platforming problem later.

8. Evaluate the vendor’s reputation

Firms generally have two ways to assess a vendor’s reputation. The first is to review the vendor’s client list and case studies, which provide evidence of outcomes and experience with comparable firms. The second is to seek external validation through industry analyst reports such as Chartis RiskTech Quadrants, peer review platforms like G2, and recognized security and data standards certifications such as ISO 27001 and SOC 2.

9. Ask for demos or tests

Successful relationships between software vendors and FIs are built over time. Firms should consider whether off-the-shelf rulesets or more customized configurations suit their specific requirements. Vendors should be able to advise on implementation and help refine how the software is configured for the firm’s risk model. Demos and sandbox-based testing are the most reliable ways to confirm a fit and avoid a costly commitment to the wrong product.

Improve efficiency with advanced payment screening

ComplyAdvantage’s Payment Screening on Mesh combines real-time sanctions data, configurable screening, and integrated case management to support firms processing payments at scale without compromising on risk.

“ComplyAdvantage has not only been able to reduce the number of false positives we see, but also the time we spend on each alert.”

Lukas Andersen, MLRO and Head of Financial Crime Risk, Inpay

FIs choosing Payment Screening on Mesh get:

- Real-time sanctions updates: Critical sanctions lists are updated in minutes, with information sourced directly from regulators and refreshed through automated systems backed by a global analyst team.

- Configurable screening: Apply different levels of fuzziness across name, BIC, and reference text fields, screen against custom allow lists and block lists that reflect internal intelligence, and tune settings without engineering support through a no-code configuration UI.

- Agentic AI augmentation: Mesh’s agentic AI, trained on a large volume of real-world data and compliance decisions, supports analysts by flagging risk that might otherwise be missed and accelerating routine case work that does not require human judgment.

- Integrated data, screening, and case management: A consolidated view of alerts and cases, with audit trails and configurable workflows so compliance teams can review and resolve cases efficiently.

Power a no-compromise payment experience

Find out how ComplyAdvantage can help you speed up your payment screening without compromising on risk.

Get a demoOriginally published 08 November 2024, updated 19 May 2026

Disclaimer: This is for general information only. The information presented does not constitute legal advice. ComplyAdvantage accepts no responsibility for any information contained herein and disclaims and excludes any liability in respect of the contents or for action taken based on this information.

Copyright © 2026 IVXS UK Limited (trading as ComplyAdvantage).