- Insights

- Featured Insights

Payment screening is, at its core, a sanctions control. It is the interception point where a financial institution (FI) checks a payment, and every party to it, against global sanctions lists before the money moves. The question is binary: is anyone in this transaction connected to a sanctions target? If yes, the payment cannot proceed.

That makes payment screening distinct from transaction monitoring, which analyzes activity over time to detect patterns that may indicate money laundering. Payment screening sits at the front of the rail and asks a single focused question very quickly.

In an era of instant settlement and tightening sanctions enforcement, getting this right is the difference between clearing a payment in 250 milliseconds and clearing a multi-million dollar fine. Regulators worldwide have penalized firms for screening failures, and even established institutions are not immune to flaws in their payment screening process. The seven practices below separate effective programs from the ones regulators come back to. To get there, firms need a strong understanding of what payment screening is for, the regulatory frameworks driving it, and the challenges that make it harder than ever to execute well.

Why is payment screening so important?

The primary risk a payment screening program is built to manage is sanctions breach. A single missed match can carry direct civil and criminal penalties, and repeated breaches can put correspondent banking relationships at risk, effectively cutting a firm off from the payment corridors it depends on. Sanctions enforcement bodies, including the US Office of Foreign Assets Control (OFAC), the UK Office of Financial Sanctions Implementation (OFSI), and the EU member state authorities, enforce these sanctions and have shown a willingness to pursue both firms and named individuals.

Reputation is the second exposure. Firms perceived as weak in their defenses against financial crime lose customers, lose partner appetite, and suffer business growth. In a market where regulated counterparties scrutinize each other’s controls before doing business, a public screening failure travels quickly.

It is worth noting that the broader money laundering and terrorist financing risks an FI must manage are not addressed solely through payment screening. They are addressed through transaction monitoring, customer due diligence, and adverse media screening, which work alongside payment screening as part of a complete anti-money laundering and combatting the financing of terrorism (AML/CFT) compliance program. Payment screening covers the sanctions interception layer; the other controls cover the rest.

The regulatory picture for payment screening

Regulators worldwide have built increasingly specific frameworks around sanctions enforcement and the payment infrastructure that screening sits on top of. The most prominent rules affecting payment screening today include:

- The EU sanctions and payments framework: Firms operating in or through the EU must screen against the EU Consolidated List, with penalties enforced by individual member states. TheEU Instant Payments Regulation (IPR) requires PSPs to process in-scope SEPA Instant euro transfers within 10 seconds, prohibits transaction-level sanctions screening on those transfers, and instead requires payment service providers to screen their customer base against EU sanctions lists at least daily. The Payment Services Regulation (PSR) and Third Payment Services Directive (PSD3), agreed in late 2025 and expected to enter into force in mid-2026 with a transition period before full application, will further tighten the operational requirements around all EU payments. TheEU AI Act classifies AML and sanctions screening tools as high-risk, meaning automated screening decisions will need to be explainable when those obligations apply from August 2026.

- The US sanctions enforcement framework: Sanctions enforcement is administered by OFAC under statutes including the International Emergency Economic Powers Act, with civil and criminal penalties for breaches of the Specially Designated Nationals (SDN) list and the sectoral sanctions programs. The introduction of the FedNow service has brought 24/7 instant settlement to US payment rails. Faster infrastructure does not reduce the obligation to screen against OFAC lists; it makes meeting that obligation in real time considerably harder.

- The UK sanctions and payments framework: OFSI enforces sanctions breaches under the Sanctions and Anti-Money Laundering Act 2018, with the UK Sanctions List the single authoritative list of UK sanctions designations since 28 January 2026. The Payment Services Regulations 2017 provide the broader operational framework for PSPs.

Adjacent fraud and consumer protection rules, including the UK mandatory reimbursement for authorized push payment (APP) scams and the EU Verification of Payee requirement, sit alongside sanctions obligations but are addressed through different controls. Given the precision and speed demanded across all of these frameworks, a real-time, automated, and explainable payment screening process is now a critical component of a compliant financial operation.

What are the most common challenges in payment screening?

Balancing customer expectations with regulatory obligations is the core challenge for FIs in payment screening. Customers demand instant, seamless transactions, but a set of evolving pressures makes this harder than ever to deliver:

- Meeting customer expectations in an instant world: The SEPA Instant Credit Transfer scheme has set the standard for real-time cross-border payments in Europe, with real-time payment transactions in EU member nations projected to reach 34.2 billion by 2027, up from 13.2 billion in 2022. Inefficient screening and high false positive rates prevent firms from delivering the experience customers now expect.

- Modernizing data and technology: The global transition to the ISO 20022 messaging standard is a significant technical hurdle. Major networks including SWIFT will soon reject payment instructions containing unstructured data, prompting firms to invest in technology that can process structured XML data in real time.

- Ensuring AI transparency and explainability: The EU AI Act classifies AML and sanctions screening tools as high-risk, imposing strict transparency requirements. Opaque or “black box” models that cannot explain their decisions are no longer compliant. Firms must be able to justify any automated decision to flag or clear a payment, which raises the bar for model governance.

- Avoiding sanctions breaches under faster settlement: Real-time payment rails compress the time available to screen, and the financial consequences of a missed match are severe. Beyond direct OFAC, OFSI, or EU penalties, repeated breaches put correspondent banking relationships at risk, which can cut a firm off from the corridors it relies on.

- Navigating an evolving sanctions landscape: Sanctions designations move at the pace of geopolitics, with major lists updated multiple times a week and sometimes daily. The creation of the EU’s Anti-Money Laundering Authority (AMLA) and the continued expansion of programs under OFAC and OFSI mean firms need screening systems that can ingest updates within minutes, not hours.

Adapt to the changing financial landscape of Europe with our expert guide to the AML challenges and opportunities of SEPA instant payments.

A guide to financial crime and SEPA instant payments

7 ways to enhance your payment screening process

Regulatory feedback for firms guilty of payment screening failures has emphasized the importance of adapting compliance programs to match business growth, so that they remain fit for purpose at all times. Here are seven steps that allow firms to do this:

1. Implement a risk-based approach

As a foundational point of AML compliance, the risk-based approach will be familiar to experienced compliance professionals. However, all firms should still ensure their approach is as efficient as possible by avoiding standardized, inflexible rules, instead undertaking regular business-wide risk assessments to identify which products or services, customers, and jurisdictions are likely to pose the highest AML/CFT risk. Firms should also have clear policies specifying when cases should be escalated for further review and when enhanced due diligence (EDD) is required. In practice, a risk-based approach could mean, for example, that firms screen transactions across different payment corridors using different datasets or apply varying levels of fuzziness in searches.

2. Use comprehensive data sources

Firms should screen payments against all relevant data from the jurisdictions in which they operate or hold significant exposure. That means screening against the major sanctions lists (including OFAC’s SDN list, the UK Sanctions List, the EU Consolidated List, and the UN Consolidated List), relevant adverse media sources, and global PEP databases where the risk model calls for them. Screening should cover all parties to a payment, including sender, receiver, intermediary banks, BIC codes, and reference text fields, since sanctions risk can be carried by any of them.

3. Receive updates in real-time

Access to a range of screening lists is important, but those lists are only effective if updated frequently. Major sanctions lists often receive multiple weekly or even daily updates, and a single missed designation can mean a breach. Using old data also causes false positives, slowing operations and pulling analysts onto cases that have already been resolved upstream. For an optimal solution, firms should seek a provider that can deliver sanctions and watchlist updates in near real time, so the screening engine is always working against the freshest source of truth.

4. Pair payment screening with transaction monitoring

Payment screening and transaction monitoring are complementary controls, not interchangeable ones. Payment screening intercepts transactions at the point of execution to check parties against sanctions lists. Transaction monitoring analyzes patterns of activity over time to detect behavior that may indicate money laundering or other financial crime. Most regulated firms need both, and running them on a single platform avoids the operational drag of analysts switching between siloed datasets, duplicate customer records, and disconnected case management tools.

5. Unify your compliance activities

Centralizing compliance activities within a single platform allows firms to integrate payment screening with transaction monitoring more efficiently and reduces the need for analysts to switch between siloed datasets and cases.

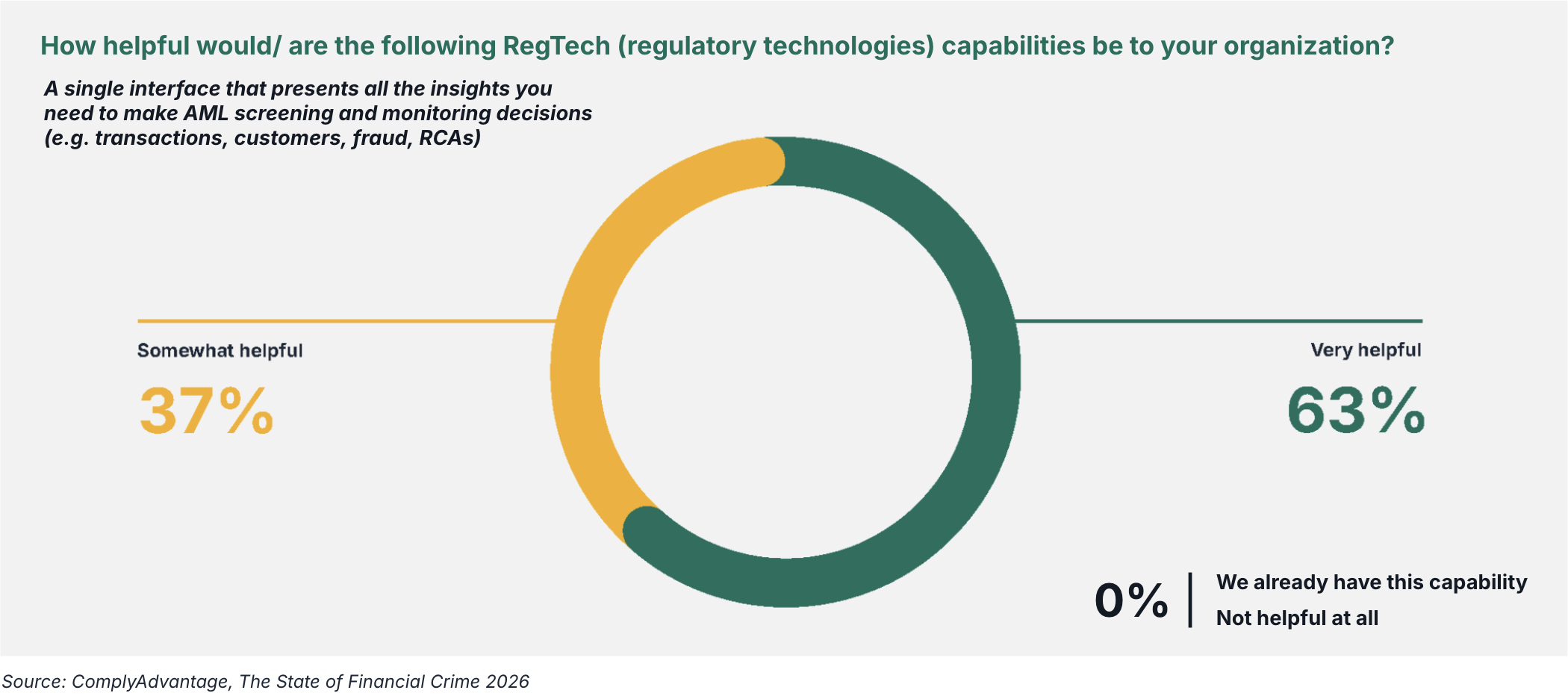

According to our 2026 State of Financial Crime survey, 100% of the 600 surveyed firms said utilizing a single interface for AML solutions would be “helpful,” yet none of them currently possess this capability, with 53% still juggling between 8 and 10 different payment screening solutions.

This paradox underscores why consolidating insights in one comprehensive, unified view of risk is crucial – especially in today’s increasingly complex regulatory landscape.

“As a cross-border payments firm, we really value ComplyAdvantage’s payment screening solution, which was a game changer for us, allowing us to centralize our payment screening and transaction monitoring activities within one team connected to one system.”

Alessio Giorgi, Head of Compliance & MLRO, Lumon

6. Maintain clear documentation

Regulators and auditors have high expectations of firms regarding record-keeping. In the event of a review, they will expect thorough documentation not only of payment screening policies and procedures but also of every decision made regarding escalated or reported transactions.

Without proper attention from firms, this critical compliance aspect can fall by the wayside, especially amid the pressure to deliver instant payments to customers. Firms should ensure records are retained and stored in a way that makes them as auditable as possible.

7. Use advanced technology to enhance screening accuracy

Dedicated AML software leveraging cutting-edge technology can offer firms a significant competitive advantage in payment screening. Artificial intelligence (AI) and machine learning (ML), in particular, have a wide range of applications in this area, from automatically refreshing screening databases to optimizing search algorithms to reduce false positives. When choosing a software solution, firms should consider their specific payment screening requirements, risk assessment, and appetite.

Advanced solutions offer powerful features to improve accuracy and efficiency. For example, a muting capability allows analysts to prevent already confirmed false positive to reappear in future case remediation and significantly reduces alert fatigue.

Firms can also create and manage custom allow lists and block lists to incorporate internal intelligence into the screening workflow. To strengthen the risk-based approach, a no-code configuration UI empowers compliance teams to adjust fuzziness settings themselves, calibrating risk tolerance without needing engineering support.

Real-time Payment Screening with ComplyAdvantage

ComplyAdvantage’s real-time Payment Screening on Mesh solution enables firms to automatically screen payments against global sanctions and watchlists so they can block or flag high-risk transactions before they are processed. Built for the era of instant payments, our solution delivers:

- Unmatched speed and scale: Screening transactions at industry-leading speed in under 250 milliseconds (ms) at P90 latency, with a throughput of 100+ transactions per second (TPS).

- A unified view of risk: Integrating solutions for Customer Screening, Ongoing Monitoring, Payment Screening, and Transaction Monitoring into a single, cohesive environment to break down data and operational silos.

- Proprietary risk intelligence: Our connected graph architecture goes beyond simple name-against-list screening by detecting and modeling the complexity of real-world risk, with critical sanctions lists updated in minutes.

- Agentic AI augmentation: Leveraging agentic AI trained on a massive volume of real-world data and compliance decisions, designed to work faster and more efficiently than a human analyst to find risk that might otherwise be missed.

“ComplyAdvantage’s solution is exactly what we were looking for. The results have been accurate monitoring and the ability to stop specific transactions in real time. We are now confident that all transactions are screened and monitored, and we are aware of many more transactions that require further investigation.”

Toh Hwee Min, MLRO at Tazapay

Discover integrated, real-time AML compliance with Mesh

A cloud-based compliance platform, ComplyAdvantage Mesh combines industry-leading AML risk intelligence with actionable risk signals to screen customers and monitor their behavior in near real time.

Get a demo

Originally published 21 November 2024, updated 19 May 2026

Disclaimer: This is for general information only. The information presented does not constitute legal advice. ComplyAdvantage accepts no responsibility for any information contained herein and disclaims and excludes any liability in respect of the contents or for action taken based on this information.

Copyright © 2026 IVXS UK Limited (trading as ComplyAdvantage).