- Insights

- Featured Insights

While it may seem intuitive that not all customers pose the same risk, identifying an effective way to assess and categorize these risks – and adapt to changes over time – is an ongoing challenge for compliance teams.

This article explores common challenges with dynamically assigning a customer risk rating that we encounter in our conversations with customers and outlines how risk scoring in the ComplyAdvantage Mesh platform solves these challenges.

This article is part of a series on the capabilities of the ComplyAdvantage Mesh platform. Rather than being a dedicated risk-scoring solution, Mesh is designed to provide a 360-degree view of risk in a single platform. Links to the rest of the series are available at the end of this article.

What is AML risk scoring?

An AML risk score refers to the level or category assigned to customers based on various potential factors. These may include a customer’s country of residence, profession, or the products they are using. To be truly effective, risk scoring must be dynamic, as a customer’s level of risk may rise and fall over time based on new information or behavioral changes.

How does effective risk scoring help with AML compliance?

When implemented effectively, customer risk scoring helps compliance professionals prioritize the greatest potential threats to their business. For example, a high-risk customer will likely require greater due diligence and a review by more senior analysts or team leads. By contrast, lower-risk clients may present risk signals that can be analyzed more quickly or in bulk with other similar cases. An AML risk scoring model can also automatically filter out prospective clients at onboarding who present an unacceptable level of risk to the business, again saving valuable analyst time.

Common challenges in implementing risk scoring for AML

When we talk to financial institutions about AML customer risk scoring, common challenges include a lack of risk scoring altogether, overly manual risk scoring, or the tools built for risk scoring being designed in-house. Behind these challenges sit several factors:

- The time taken to develop risk models—in some cases, teams have taken more than three months.

- An inability to prioritize or allocate compliance resources efficiently.

- Risk decisions are based on subjective judgments rather than data.

- An inability to monitor and detect risk changes among an existing customer base.

- Applying a one-size-fits-all approach that disregards risk levels.

- A failure to segment customers based on their risk levels.

- Human errors, data losses, and/or a lack of integration.

- The lack of a targeted approach to identifying, assessing, and mitigating risk.

AML risk scoring models: The ComplyAdvantage solution

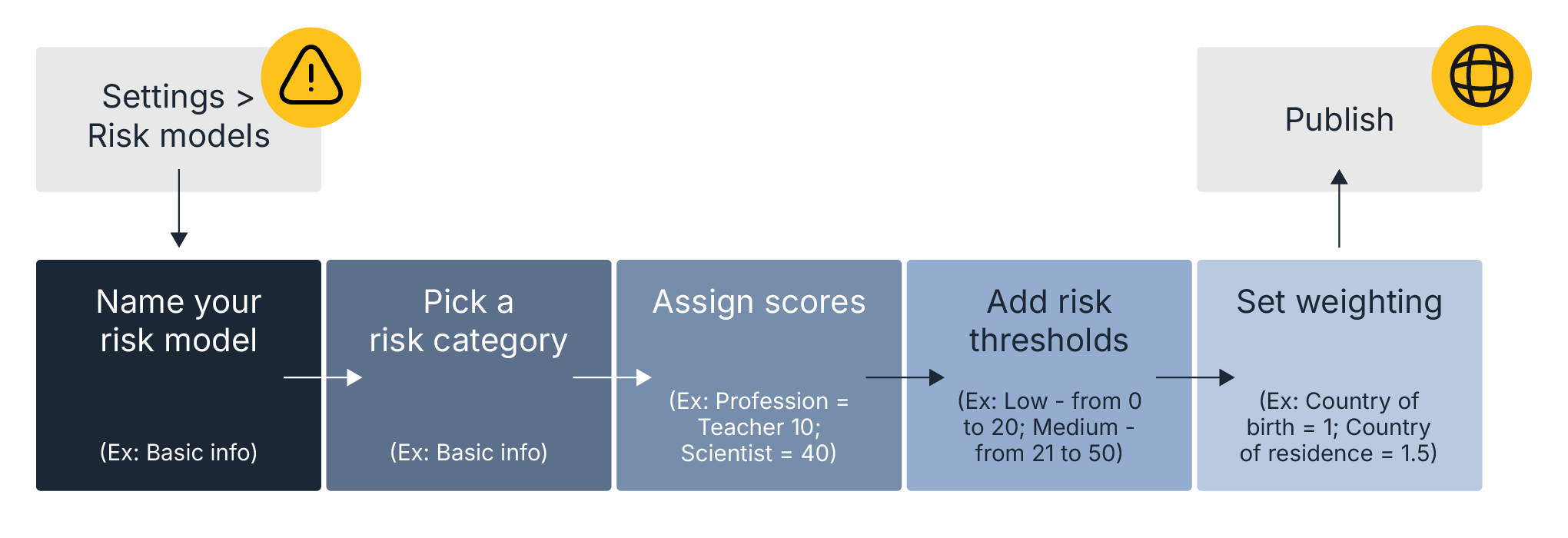

The ComplyAdvantage Mesh platform offers highly configurable risk scoring so firms can build models specific to the risks of their organization and the particular products and services they offer. Here’s how it works:

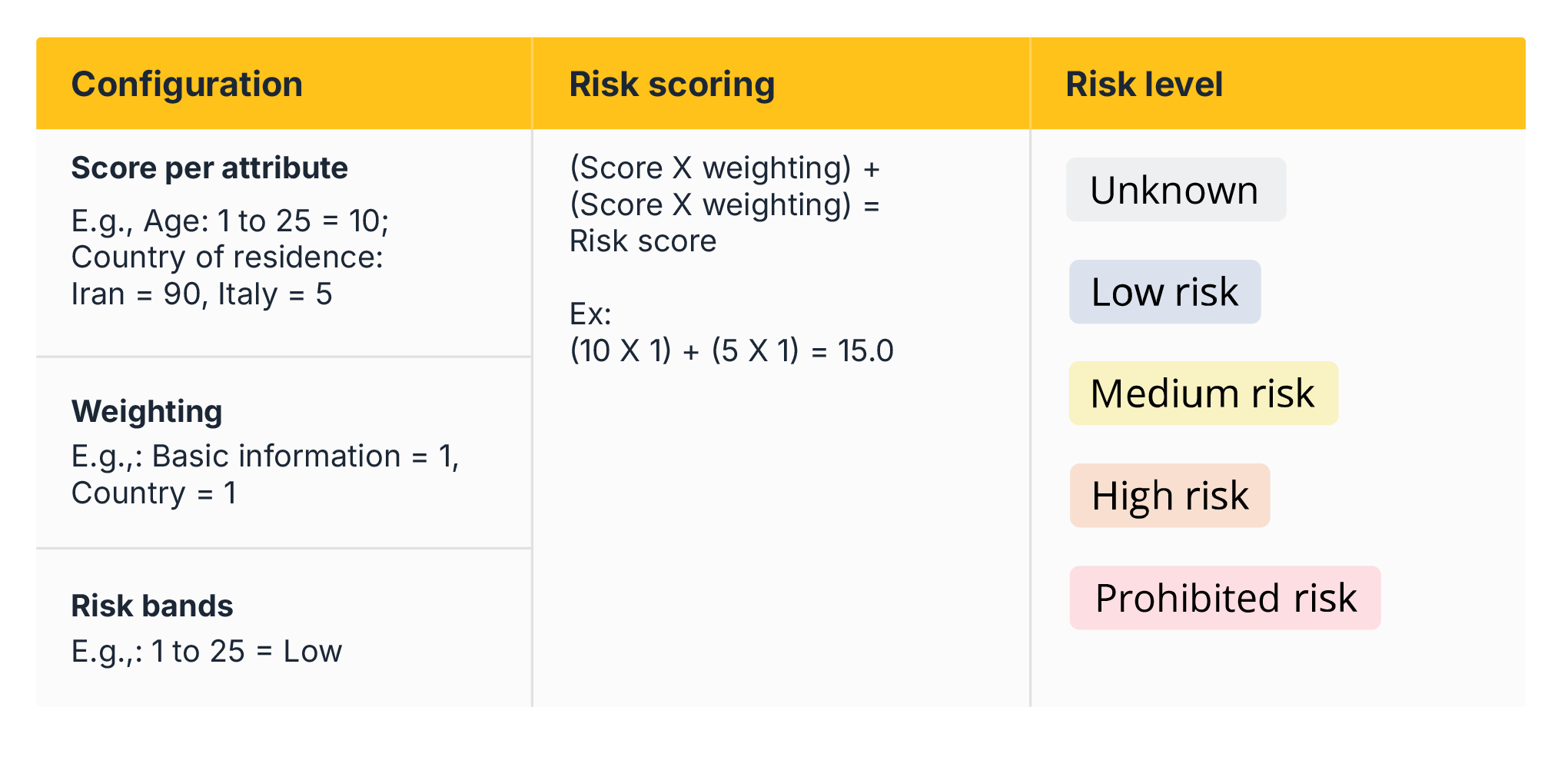

An important part of dynamic risk scoring is the weighting of different factors. Age, country of residence, profession, etc., are all important but may not be considered equal factors. This is how the Mesh platform allows compliance leads to weigh their risk scores, using the hypothetical example of John Smith. Mr Smith was born on January 1, 2000, in Italy.

The diagram above shows that Mr Smith is given a ‘low’ AML risk score using the example attribution model.

Best practices for implementing an effective AML risk scoring with ComplyAdvantage

Underlying this risk model approach are five core principles that have shaped the development of our risk-scoring solution:

- A fully automated process. Manual elements will cause risk scores to become outdated, with risks slipping through the cracks and low-risk customers facing a disproportionate level of due diligence.

- Minimal levels of coding required. Ideally, compliance teams should be able to build and adapt risk models without engineers’ support. The need for custom coding will add costs and reduce the speed at which updates can be made.

- The ability to link customer reviews back to the business-wide risk assessment. Factors such as country, professional, product, channel, and more should be included in alignment with the firm’s overall risk-based approach. This is especially important when weighing the importance of individual risk factors.

- Flexible workflows that ensure, for example, that prospective customers with prohibited statuses are automatically skipped at onboarding. Automatic workflows also enable firms to quickly onboard customers where no results are shown and prioritize cases that sit in between where an analyst needs to assess the level of risk.

- Scores and methodologies are easily visible and explainable. In addition to assessing customers at the micro-level, macro-level reporting via dashboards helps firms assess risk at the customer population level and supports teams in meeting their regulatory requirements.

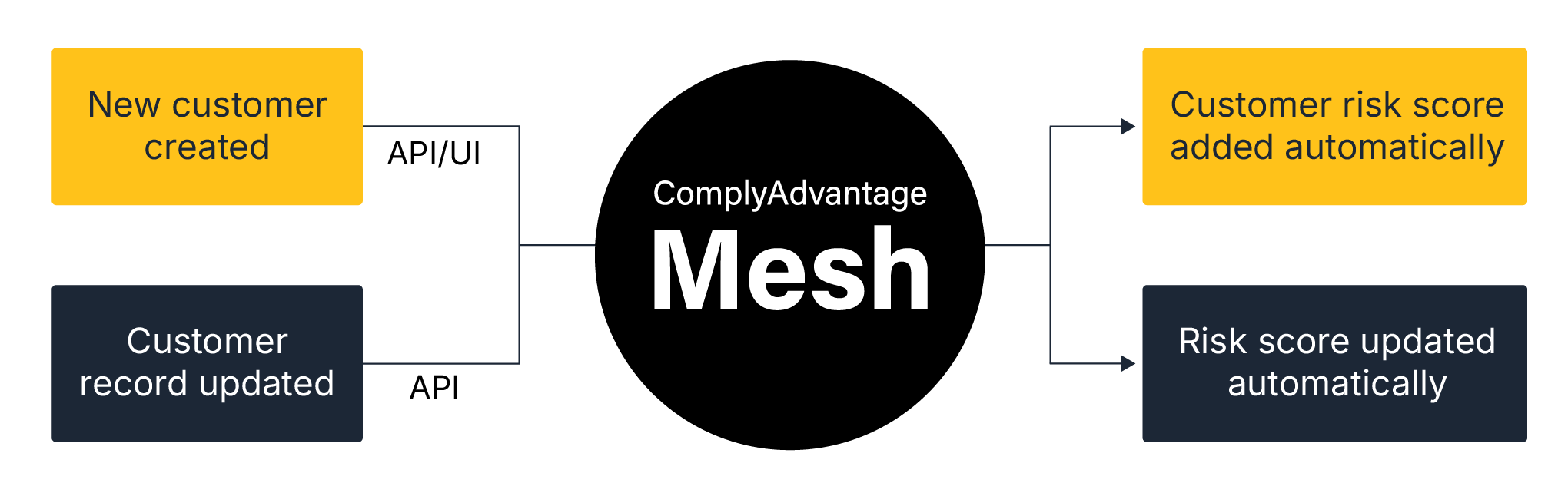

Why does ComplyAdvantage Mesh offer dynamic AML risk scoring?

Risk scoring in the ComplyAdvantage Mesh platform has been built with the needs of compliance leaders in mind. The diagram below shows how risk scores are updated.

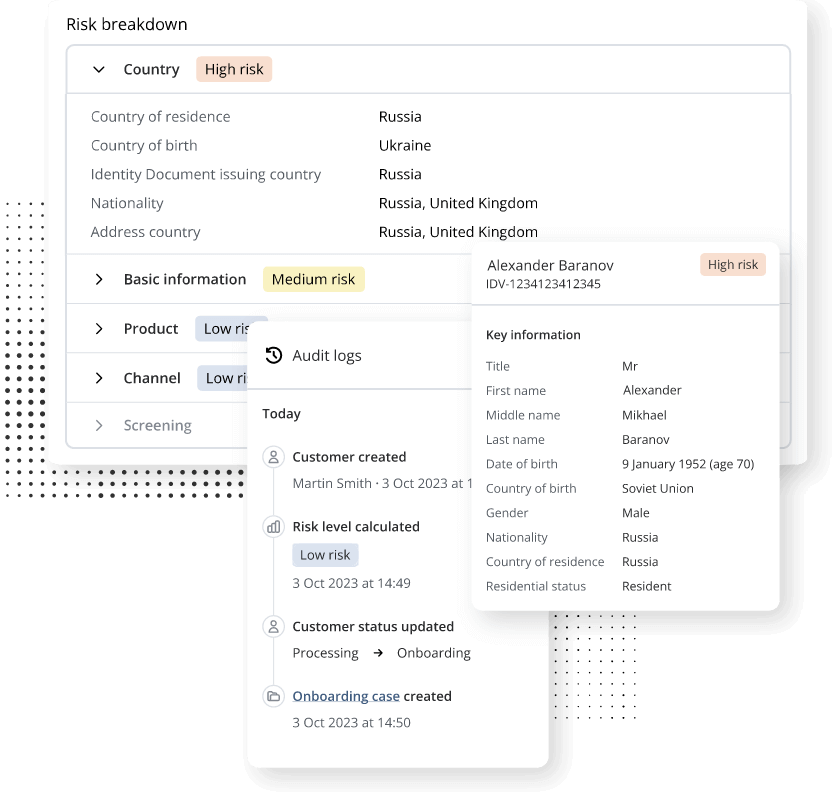

The categories firms can configure in their risk-scoring models are aligned with the business-wide risk assessment:

- Basic information

- Screening

- Geography

- Product

- Channel

Scores and weightings can be set across all these categories. In addition, Mesh offers:

- Total automation, with risk scoring enabled via API.

- Unlimited risk models.

- Insightful reporting to help firms understand how customers contribute to overall business risks.

- Customer support and guidance to enable firms to build models based on industry best practices.

Find out more about ComplyAdvantage Mesh by reading the other articles in the series:

Explore how ComplyAdvantage Mesh gives firms a 360-degree view of risk

Find out more about how Mesh combines industry-leading AML risk intelligence with actionable risk signals to screen customers and monitor their behavior in near real-time.

Learn moreOriginally published 21 January 2025, updated 27 January 2025

Disclaimer: This is for general information only. The information presented does not constitute legal advice. ComplyAdvantage accepts no responsibility for any information contained herein and disclaims and excludes any liability in respect of the contents or for action taken based on this information.

Copyright © 2026 IVXS UK Limited (trading as ComplyAdvantage).