- Insights

- Featured Insights

Transaction screening is part of a robust anti-money laundering and counter-terrorist financing (AML/CFT) framework. Along with customer identification and verification, transaction monitoring, and regulatory reporting, transaction screening helps firms engage in sound due diligence and compliance processes.

But what’s involved in effective transaction screening? How does it differ and overlap with a firm’s overall compliance process? And how can up-to-date technology enable it?

Discover the ins and outs of transaction screening, what separates it from transaction monitoring – and the best way to ensure an effective process.

What is transaction screening?

Transaction screening analyzes transactions for suspicious or prohibited activity before they are approved. If analysis confirms illicit or excessively risky activity, the transactions are stopped. This is necessary to filter out blatant attempts to get around regulations such as international sanctions. It also contributes to a layered, risk-based approach to AML/CFT due diligence.

Transaction screening vs transaction monitoring

Transaction screening looks at individual transactions, such as payments, before they’ve been approved to stop especially high-risk activity. For example, a transaction to a sanctioned entity or for prohibited goods can be denied regardless of the customer’s past activity.

On the other hand, transaction monitoring analyzes transaction patterns for suspicious activity after they’ve been approved. Some transactions may not be obviously high risk on their own and pass the screening process. Yet, if they are part of a wider network of suspicious activity, their relationship to past transactions can alert monitoring teams to investigate further.

Transaction screening vs payment screening

Payment screening, while a type of transaction screening, only deals with payments before they are processed. On the other hand, transaction screening may deal with other types of transactions, from payments to cash deposits, withdrawals, and ACH transactions.

The steps each screening process follows is similar, but can vary based on the specific risk factors involved in the transaction types being screened.

Transaction screening and AML regulations

Regulators generally focus on a risk-based approach to AML/CFT rather than dictating tools and processes at a granular level. Still, transaction screening is a vital component of any sound program.

Regulators require a customer due diligence program that enables firms to have sufficient customer information and to identify and report suspicious activity. Firms found to be lacking in customer due diligence can be penalized. For example:

- In the United States, the Financial Crimes Enforcement Network (FinCEN) fined a major firm $140m for failing to implement an AML program meeting the minimum Bank Secrecy Act (BSA) requirements.

- In the European Union, the French Autorité de Contrôle Prudentiel et de Résolution (ACPR) fined a firm €1.5m for failures that included insufficient customer due diligence (CDD) processes and deficient procedures for investigating suspicious payments.

- In the United Kingdom, the UK Gambling Commission fined a firm £9.4m for AML shortcomings, including a failure to establish customers’ source of funds (SOF).

A lack of sound screening could lead to CDD failures, including sanctions violations. This, in turn, could lead to regulatory penalties.

The Role of Technology and Talent in Transaction Screening

Discover how firms are investing to improve transaction screening processes and manage risk in an increasingly complex environment.

Download NowTransaction screening red flags

When teams review transaction alerts during screening, they look for red flags that could indicate illicit or risky activity. These can include signs that the transaction:

- Is being sent to a sanctioned location.

- Involves possible illicit goods, such as dual-use goods.

- Is unusually large for the account.

- Is atypical for the account’s expected activity – such as business transactions on a personal account or vice-versa.

- In some other way falls outside the firm’s accepted risk appetite or policies.

- The sender or recipient is sanctioned or has associated negative news.

- Other parties in the payment may be associated with sanctions (e.g. the bank of the beneficiary).

Red flags are meant to be initial indicators that further investigation is needed. When analysts encounter any of the above red flags, they will generally initiate a deeper review. Sometimes, an activity that initially seemed suspect will be labeled legitimate after further clarification of the context. Other times, a payment will be confirmed as illicit (for example, if it involved sanctioned entities) – or at least high-risk enough to be stopped.

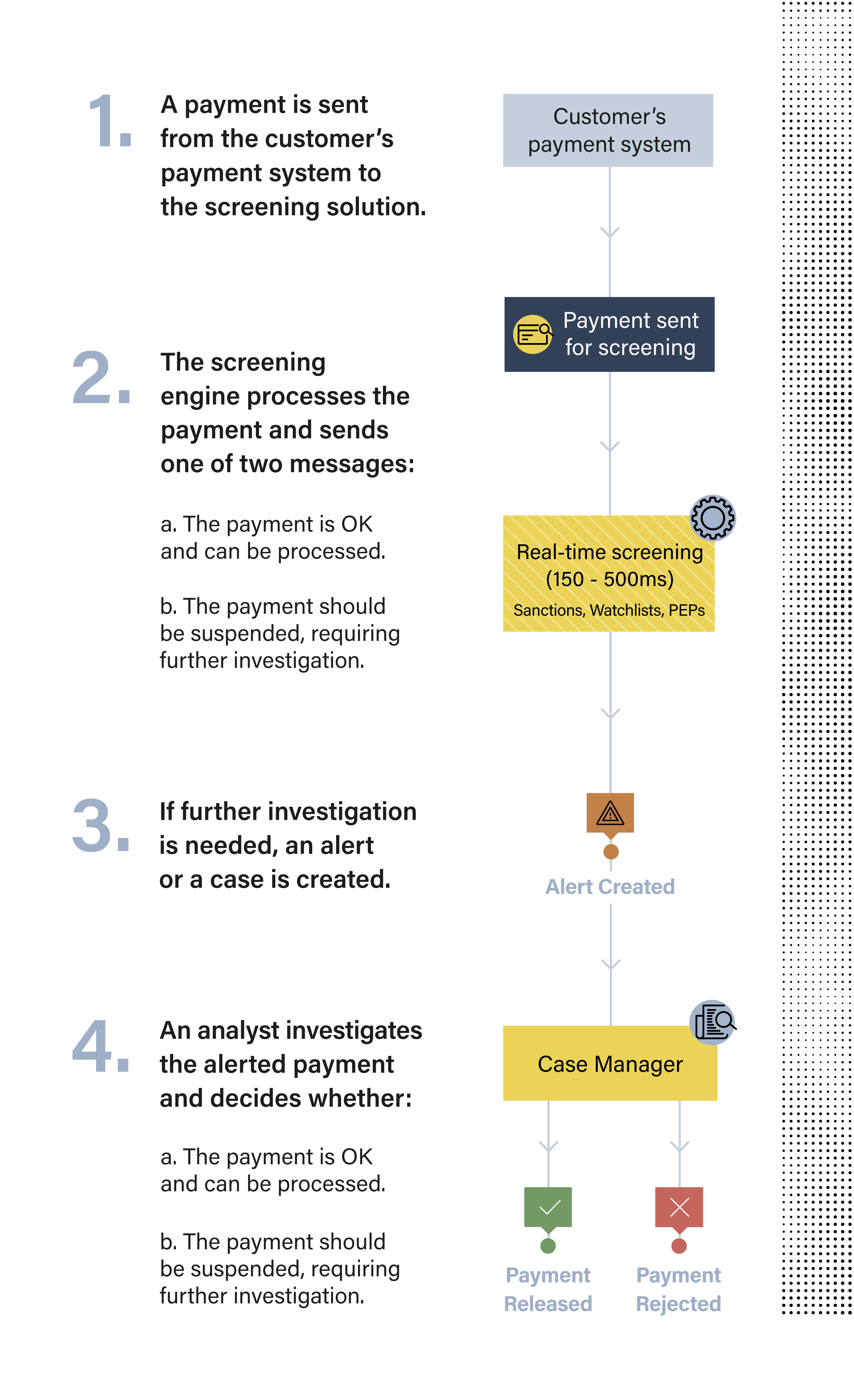

What is the AML transaction screening process?

Each transaction passes through a screening process before being approved. The exact steps may vary between institutions, depending on their policies and the tools they use. However, the process will often follow a pattern like this:

Payments that make it through the screening process are approved but are usually only looked at individually. After approval, those transactions are subject to ongoing monitoring alongside other transactions to ensure approved payments aren’t part of a larger pattern of suspicious activity.

Transaction screening benefits

Regulators encourage firms to maintain appropriate transaction monitoring, but transaction screening is equally important owing to the following benefits:

- Creating a barrier to criminal networks seeking to evade sanctions – It’s crucial for firms to take steps to prevent transactions that are in outright violation of regulations.

- Reducing the number of alerts facing transaction monitoring – By stopping transactions that can be deemed unacceptable outright, payment screening teams free their transaction monitoring counterparts to investigate more pattern-based illicit activity.

- Improving compliance and risk management by implementing a multi-layer due diligence process – Effective AML/CFT depends on a coordinated, multi-layer approach from customer verification to ongoing due diligence. When calibrated according to a precise risk profile, the two-step screening and monitoring process helps firms mitigate transaction risks holistically. For this to work well, it’s essential that payment screening and monitoring teams are in communication and can alert one another of risky activity. Since each team looks at payments from a different angle, they may see things the other misses.

Transaction screening challenges

Firms can encounter transaction screening challenges related to outdated systems, unreliable or poorly processed data, and overwhelmed teams facing unrealistic screening workloads. These can include:

- Backlogs caused by false positives – When too many false positives are generated, they can congest queues and take away valuable analyst time from true positives. This translates to less accurate screening and analyst burnout.

- Unclear alert data – Analysts often face alerts that don’t clearly explain the data that triggered them. This leaves teams without the context needed to perform an adequate investigation. This, in turn, could result in too much time spent on low-risk activity – or a failure to recognize transactions that should be stopped.

- Out-of-date sanctions data – Firms may stop allowable transactions or permit illicit ones if their data is not closely synced with regulatory updates.

- Slow screening times – Firms often encounter delays of up to a day or longer processing individual alerts. This already impacts legitimate customer satisfaction. Yet with the advent of faster payments, customers will be expecting quicker processing. At the same time, ISO 20022 will mean an increase in incoming payment data.

To keep pace, firms will need solutions that are not slowed down by inaccurate data or an inability to identify targeted risks. Even expert analysts are hampered in curbing a firm’s AML risks without adequate screening tools.

Mitigate AML risks with automated transaction screening solutions

To stay ahead of growing financial crime risks and regulatory requirements, firms must provide robust analyst support for alert investigations. This includes ensuring their transaction screening system provides clear, accurate, and comprehensive data for investigations.

ComplyAdvantage’s payment screening solution can help firms reach this goal. Using data-optimized screening algorithms, most payment transactions can be processed without delay. This is because screening lists can be tailored to a firm’s unique and changing risks, focusing on relevant risks without clogging analyst workflows with irrelevant ones. At the same time, sanctions lists are regularly updated straight from regulator sources. Firms can integrate these updates into their screening process within as little as an hour. The system supports fast payments and ISO 20022, ensuring firms are ready for the payments future.

Demo Request

See how leading companies are screening against the world's only real-time risk database of people and businesses.

Request a DemoOriginally published 06 October 2023, updated 13 May 2024

Disclaimer: This is for general information only. The information presented does not constitute legal advice. ComplyAdvantage accepts no responsibility for any information contained herein and disclaims and excludes any liability in respect of the contents or for action taken based on this information.

Copyright © 2026 IVXS UK Limited (trading as ComplyAdvantage).