- Insights

- Featured Insights

An ultimate beneficial owner (UBO) is someone who ultimately owns or controls a company and benefits from its financial transactions. Because UBOs sometimes seek to remain anonymous, often through a complex chain of corporate infrastructure, they may not be immediately identifiable. Therefore, it’s crucial for financial institutions (FIs) to understand the intricacies of beneficial ownership and implement appropriate measures to accurately identify UBOs, thereby mitigating risks associated with anonymity.

When FIs onboard businesses and other entities as customers, they must have protocols in place to ensure they know exactly who they are beginning a business relationship with. This means identifying an account’s UBO.

Why is it important to conduct UBO checks?

When criminals launder illegal funds, one way they try to avoid detection by firms’ anti-money laundering/countering the financing of terrorism (AML/CFT) measures is by concealing their identities. To do this, they often use proxies such as shell companies to transact on their behalf.

Although shell companies are not illegal outright, criminals often use them to disguise illegal funds and gain access to legitimate financial systems. By properly investigating ultimate beneficial ownership, firms can mitigate the AML/CFT risks posed by the misuse of shell companies and similar financial crime typologies. UBO checks are a common regulatory requirement, meaning failure to carry them out can carry financial or criminal consequences.

Ultimate beneficial ownership and AML regulations

AML regulations in various jurisdictions include definitions and requirements around beneficial ownership. While definitions of UBO can vary, they typically involve a minimum ownership threshold of shares in a company. The Financial Action Task Force (FATF) guidance on UBOs, followed in many jurisdictions’ regulations, recommends that this threshold not exceed 25%, meaning that anyone who owns a stake in an entity exceeding this threshold should be considered its UBO. Some further key points to understand in different countries are:

- US UBO regulations: Under the Anti-Money Laundering Act (AMLA), the US has a centralized beneficial ownership database, the Corporate Transparency Act (CTA). Reporting companies must submit beneficial ownership information and documentation, including a UBO’s name, date of birth, address, and the unique identifying number of an acceptable identification document, to the Financial Crimes Enforcement Network (FinCEN).

- UK UBO regulations: Officially, UBOs are known in the UK as ‘persons with significant control’ (PSCs). Businesses must declare these on their PSC registers and submit them to Companies House, the body responsible for incorporating UK businesses. Additionally, the UK introduced the Register of Overseas Entities (ROE) under the Economic Crime (Transparency and Enforcement) Act 2022, meaning any foreign entity owning UK land must disclose its beneficial owners to Companies House.

- EU UBO regulations: The EU’s ‘new’ Sixth Anti-Money Laundering Directive (6AMLD) has broadened its definition of UBOs by allowing a lower ownership threshold of 15% for higher-risk companies. The directive, driven by the Anti-Money Laundering Regulation (ALMLR), also states that family ties can be considered when deciding who controls an entity. Trusts and similar legal arrangements are now required to register their UBOs, as are businesses.

- Singapore UBO regulations: Singapore maintains the Register of Registrable Controllers (RORC) as a centralized UBO database. All private companies, as well as private partnerships and non-profit organizations (NPOs), must submit information on their UBOs for inclusion on this register.

How to conduct effective UBO checks

1. Collect identifying information

At the onboarding stage, FIs should ask prospective customers for essential information to establish their UBOs. This includes company names, registration numbers, addresses, and the names of individuals in senior management roles. This data should be backed up with appropriate documentation to verify it. Firms should research anyone – both natural and legal persons – with an interest or shares in the company.

2. Confirm UBO status

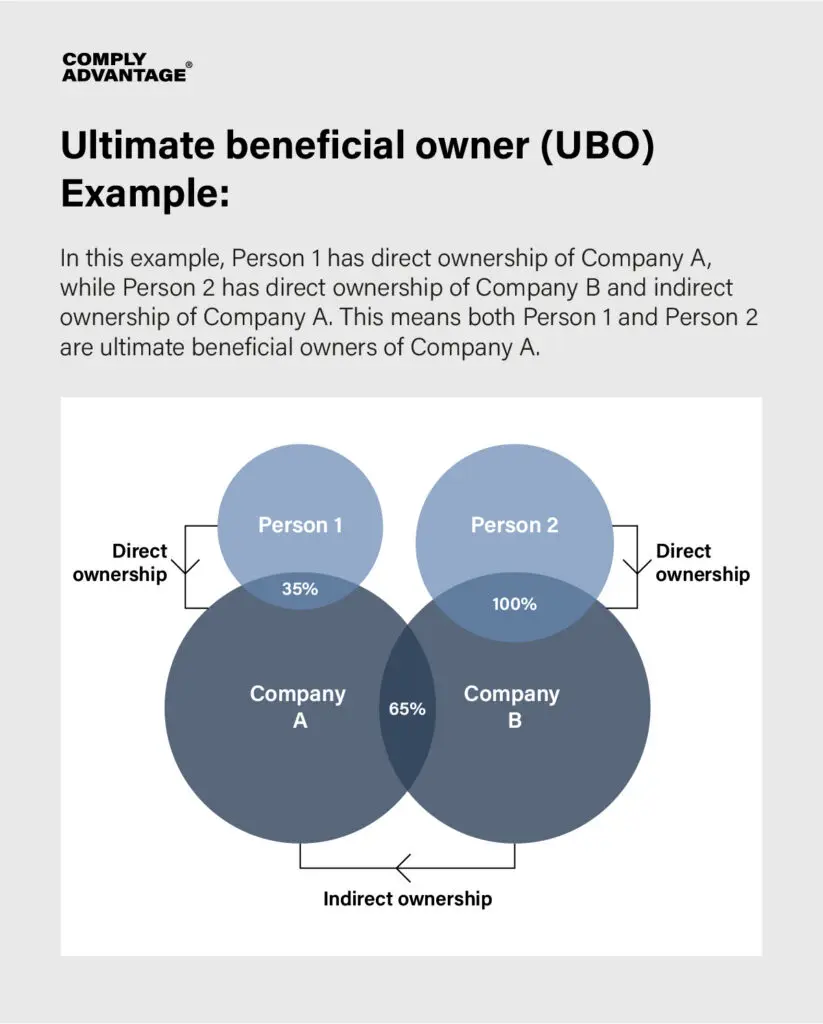

Using this information, FIs should determine who to define as a UBO. This will, as a first step, involve checking individuals against ownership thresholds. It is important to note that these thresholds apply both to direct ownership, where a UBO owns shares in a company itself, and indirect ownership, where a UBO owns shares in an additional entity that controls the company in question. Firms should also bear in mind that an entity can have more than one UBO.

However, ownership thresholds are only one route toward establishing beneficial ownership. There are situations in which persons who do not meet a threshold can exercise control over a company. The FATF gives several other examples of UBOs, including:

- Persons with the power to appoint the majority of senior management.

- Creditors are able to control a company through the terms of a lending agreement.

- Anyone appointed to a position within a company that allows them to make major strategic decisions.

- Minority shareholders who retain control over a company through differential voting rights.

3. Conduct customer due diligence on UBOs

Once firms have identified an entity’s UBOs, they must carry out an appropriate level of customer due diligence (CDD) on them. In practice, this should involve:

- Politically exposed person (PEP) screening: PEPs can present an elevated AML risk due to their positions of power and influence, making them potentially more susceptible to corruption, bribery, and other forms of financial misconduct. Because of this, PEPs may seek to use shell companies to conceal their identities. Therefore, firms should screen customers to establish their PEP status and consider applying enhanced due diligence (EDD) measures to assess the associated risks

- Sanctions screening: Individuals or entities subject to international sanctions may seek to use shell companies to evade these measures and access financial services. Accordingly, firms should screen high-risk customers against the relevant sanctions lists and implement robust monitoring systems to detect circumvention attempts.

- Adverse media screening: News stories may indicate that customers are involved in UBO-related money laundering offenses before official sources reveal this information. Firms should implement negative news screening to flag any stories involving their customers and align their adverse media categories with the FATF’s risk typologies to ensure potential money laundering risks are identified and managed in accordance with global standards.

In addition to implementing these onboarding measures, companies should also conduct continuous monitoring of transactions. This practice is crucial for identifying shell companies by detecting unusual transaction patterns or transactions involving high-risk countries.

A Guide to the Essentials of Anti-Money Laundering

Learn more about how to meet your compliance obligations, both at onboarding and beyond.

Download your copyBest practices for managing UBO risks

Some UBOs represent a higher risk of money laundering. This can be because of:

- A positive alert on any of the screening measures listed above.

- A UBO’s location is in a high-risk jurisdiction, such as a country on the FATF ‘grey’ or ‘black’ lists, especially if the entity they control is located elsewhere.

- The nature of the company’s business or the UBO’s occupation (businesses such as travel agencies, unregulated charities, and casinos should be assigned a higher risk level).

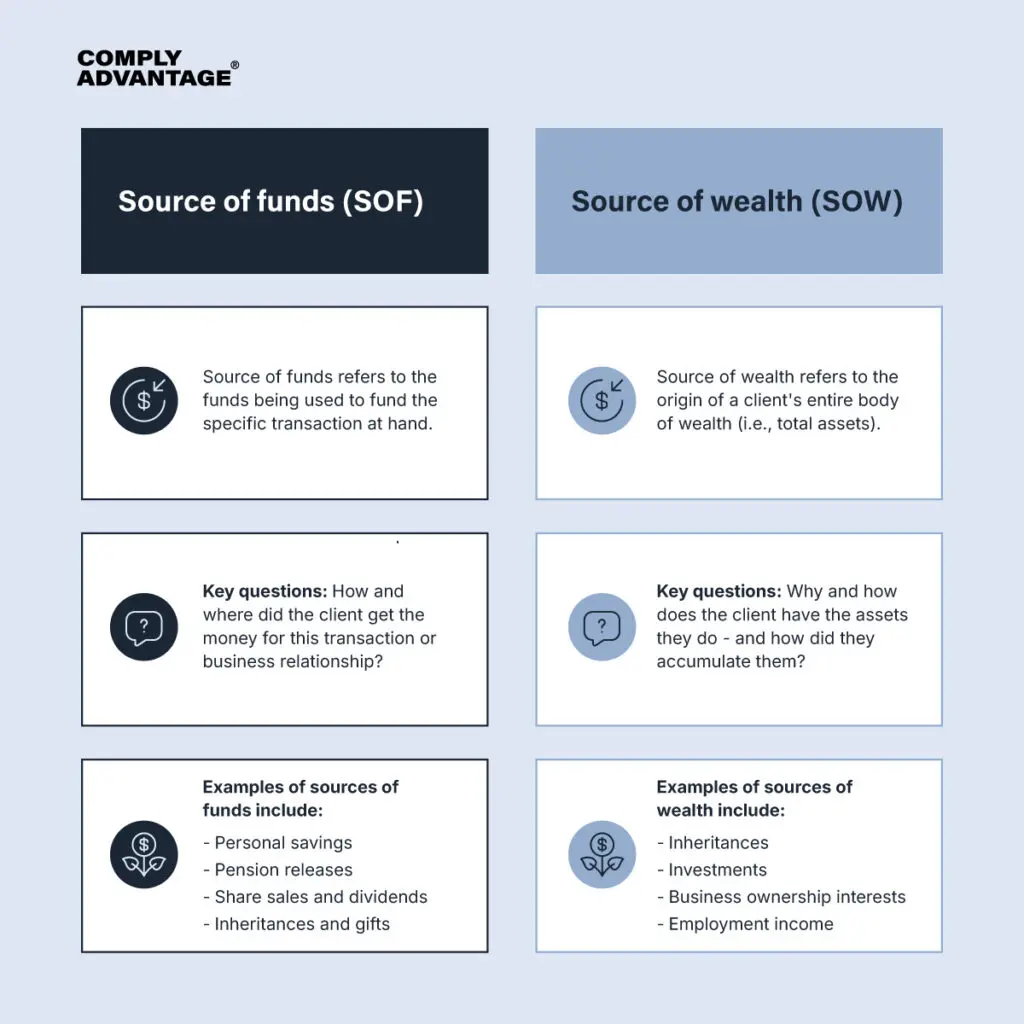

Firms should undertake further checks, known as EDD, on higher-risk UBOs. An important part of EDD consists of source of funds (SOF) and source of wealth (SOW) checks: firms conduct these to understand how a company or its UBO has obtained its financial assets and investigate any inconsistencies. Firms can also ask for further details on the purpose of the UBO’s intended business relationship with them, or for more frequent reports on a company’s ownership as a condition of the relationship.

In cases where a UBO presents a clear risk of money laundering or terrorist financing, an FI should not onboard them or the entity they control and must report any suspicious activity to the relevant authorities.

Advanced AML solutions for UBO checks

ComplyAdvantage’s specialist AML solutions include intuitive features to help firms identify and mitigate UBO-related risks, including:

- Company Screening and Customer Screening: Market-leading proprietary databases enable firms to efficiently screen for adverse media, PEP status, and sanctions or enforcement actions, allowing them to assess risk levels and take appropriate action.

- Transaction Monitoring: Our transaction monitoring solution features an extensive rules library of AML/CFT typologies, complete customization, and scalability to billions of transactions, helping FIs easily detect suspicious transaction patterns.

- Ongoing Monitoring: By continually monitoring customer and company information, firms can quickly capture and act on changes to their risk profiles.

Manage UBO risks with enhanced company screening

Mesh Company Screening allows businesses to protect themselves from financial crime risks with market-leading software and risk intelligence.

Get a demoOriginally published 04 April 2015, updated 26 March 2026

Disclaimer: This is for general information only. The information presented does not constitute legal advice. ComplyAdvantage accepts no responsibility for any information contained herein and disclaims and excludes any liability in respect of the contents or for action taken based on this information.

Copyright © 2026 IVXS UK Limited (trading as ComplyAdvantage).