- Insights

- Featured Insights

The Financial Action Task Force (FATF) is an intergovernmental organization that monitors global money laundering (ML) and terrorist financing (TF) trends. The FATF collaborates with its member states and regional organizations to develop a legal, regulatory, and operational framework for combating these threats. As part of its efforts, the FATF maintains a black list, officially known as High-Risk Jurisdictions subject to a Call for Action, and a grey list. The grey list includes countries that have committed to addressing strategic deficiencies in their anti-money laundering and countering the financing of terrorism (AML/CFT) regimes. Given the potential regulatory risk associated with countries that do not maintain international compliance standards, financial institutions should be aware of the FATF black list and grey list countries and what that designation entails.

What is the FATF black list?

The FATF black list (sometimes referred to as the OECD black list) is a list of countries that the intergovernmental organization considers non-cooperative in the global effort to combat ML/TF. By issuing the list, the FATF hopes to encourage countries to improve their regulatory regimes and establish a global set of AML/CFT standards and norms. Black-listed countries are likely to be subject to economic sanctions and other prohibitive measures by FATF member states and international organizations.

The black list is a living document issued and updated periodically in official FATF reports. Countries are added and withdrawn from the black list as their AML and CFT regulatory regimes are adjusted to meet the relevant FATF standards. The first FATF black list was issued in 2000 with an initial list of 15 countries. Since then, the lists have been published as part of official FATF statements and reports yearly and sometimes twice yearly.

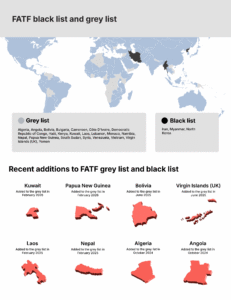

As of February 2026, the FATF black list consists of the following countries:

- Democratic People’s Republic of Korea

- Iran

- Myanmar

The FATF cites significant deficiencies in the AML/CFT regimes of the blacklisted countries and urges other countries to exercise extreme caution when doing business with firms based in these jurisdictions. While the FATF has called on its member states to “apply effective countermeasures” in any business dealings with North Korea and Iran, it has called on states to apply risk-proportionate enhanced due diligence (EDD) to Myanmar.

While it has no direct investigatory powers, the FATF monitors global AML/CFT regimes closely to inform the content of its black lists. Some observers have criticized the term “non-cooperative” about countries on the black list, pointing out that some black-listed countries may not have the regulatory infrastructure or resources to enact the FATF’s AML/CFT standards, rather than acting in defiance of international best practices.

What is the FATF grey list?

The FATF grey list, officially known as Jurisdictions Under Increased Monitoring, includes countries with deficiencies in their AML/CFT regimes. Like the black list, the grey list was created in 2000 and is updated periodically. Countries on the grey list are subject to increased monitoring and must work with FATF to improve their regimes.

To do this, the FATF either assesses them directly or uses FATF-style regional bodies (FSRBs) to report their progress toward their AML/CFT goals. While grey list classification is not as punitive as the black list, countries on the list may still face economic sanctions from institutions such as the International Monetary Fund (IMF) and the World Bank, and experience adverse effects on trade.

The grey list is updated regularly as new countries are added or as countries that complete their action plans are removed. As of February 2026, the FATF grey list includes the following countries:

- Algeria

- Angola

- Bolivia

- Bulgaria

- Cameroon

- Côte d’Ivoire

- Democratic Republic of Congo

- Haiti

- Kenya

- Kuwait

- Laos

- Lebanon

- Monaco

- Namibia

- Nepal

- Papua New Guinea

- South Sudan

- Syria

- Venezuela

- Vietnam

- Virgin Islands (UK)

- Yemen

A Guide to the FATF Grey List

The FATF grey list is among the best-known indices of higher-risk countries in the compliance industry. But how should firms respond to a grey listing in practice?

Download your copyRecent additions to the FATF grey list and black list

The FATF continuously reviews its member states’ AML/CFT performance to gauge their alignment with its regulatory guidance. The FATF has recently added the following countries to the grey list:

Algeria: In October 2024, Algeria was added to the grey list, with the country’s action plan specifying improvements around implementing risk-based supervision, establishing a framework for basic and beneficial ownership information, enhancing its suspicious transaction reporting procedures, applying financial sanctions for terrorism financing, and conducting oversight of the country’s non-profit sector.

Angola: After the June 2023 adoption of its mutual evaluation report (2023), Angola made progress on some of its recommended actions. However, the FATF has since identified deficiencies in the country’s AML/CFT regime, including its understanding of ML/TF risks, supervision of non-financial entities, low prosecution rates for criminal offenses, and delays in implementing sanctions. In October 2024, Angola was added to the grey list.

Bolivia: Since its last mutual evaluations report (MER) in 2023, it has made some progress on its recommended actions, including improving its understanding of ML/TF risks, strengthening its financial intelligence networks, and increasing its ability to investigate terrorist financing. However, this was not enough to prevent a grey listing in June 2025, and Bolivia will now work with the FATF to implement risk-based supervision of designated non-financial businesses and professions (DNFBPs), ensure beneficial ownership information is accurate and up to date, and increase ML investigations and prosecutions.

Côte d’Ivoire: Despite making progress on some of its June 2023 MER’s recommendations, such as strengthening its legal AML/CFT framework, Côte d’Ivoire was added to the grey list in October 2024. The country will continue to work with the FATF to implement its action plan, including by demonstrating a sustained increase in ML/TF prosecutions, strengthening its sanctions framework, and improving its measures to verify beneficial ownership information.

Kuwait: After its initial 2015 removal, Kuwait was re-listed in February 2026 following the country’s 2024 MER. Critical shortcomings were highlighted with its AML/CFT framework, including an inadequate understanding of TF risks and a lack of investigations into complex ML cases. The country is also tasked with improving the implementation of targeted financial sanctions to ensure assets linked to terrorism can be promptly frozen. Kuwait has committed to working with the FATF and the Middle East and North Africa Financial Action Task Force (MENAFATF) to address these strategic deficiencies.

Laos: Despite Laos’ steps to address recommendations from its 2023 MER – such as bolstering financial intelligence unit (FIU) resources and eliminating bearer shares – the FATF found significant challenges remained regarding the country’s risk assessment process, regulatory oversight, and law enforcement effectiveness. As a result, the FATF added Laos to the grey list in February 2025.

Lebanon: The FATF placed Lebanon on the grey list in October 2024, citing the country’s AML/CFT risk assessments, its approach to asset recovery, and its lack of up-to-date beneficial ownership information as areas for improvement. However, the FATF has acknowledged the social, economic, and security-related difficulties Lebanon has faced since its invasion by Israel in October 2024, and has not recommended that enhanced due diligence (EDD) or countermeasures be applied to the country.

Monaco: Monaco, which has the highest concentration of millionaires and billionaires in the world, was added to the grey list in June 2024 due to insufficient progress in combating illicit financial flows. This decision follows a January 2023 review by MONEYVAL, which found that while Monaco had made some progress in identifying ML/TF threats, significant gaps remained in its investigative and prosecutorial capabilities.

Nepal: While Nepal made legislative amendments in 2024 to align with FATF standards, the country has struggled with implementation and enforcement, particularly in financial sector oversight, prosecutorial effectiveness, and regulatory compliance. The Asia/Pacific Group on Money Laundering (APG) had previously flagged Nepal’s slow response to key recommendations from its 2022 mutual evaluation report (MER), which highlighted persistent gaps in monitoring high-risk sectors and financial crime enforcement. These shortcomings, coupled with Nepal’s historical challenges in maintaining financial transparency, led the FATF to place the country under increased monitoring in February 2025.

Papua New Guinea: Papua New Guinea was added to the grey list in February 2026, a decade after its 2016 removal. Although the country made technical improvements following its first listing in 2014, its 2024 mutual evaluation revealed significant systemic AML/CFT failures. The FATF identified significant deficiencies in criminal prosecutions for ML and in the supervision of high-risk sectors, including DNFBPs. Papua New Guinea must demonstrate a proven track record of enforcement, enhance its understanding of ML risks, and improve the effectiveness of its FIU.

Venezuela: In early 2022, an assessment team visited Venezuela to prepare the country’s MER. The team raised concerns about ML risks associated with the nation’s large informal economy, including illegal mining. They also highlighted terrorist financing threats linked to the close economic alliance between Caracas and Tehran. Consequently, Venezuela was added to the grey list in June 2024.

Virgin Islands (UK): In June 2025, the FATF tasked the British Virgin Islands with enhancing risk-based supervision of investment firms, virtual asset service providers (VASPs), and trust or company service providers (TCSPs), ensuring beneficial ownership information is available to the authorities, and systematically pursuing ML investigations, among other measures. However, the jurisdiction has made some progress since its most recent mutual evaluation report (MER), such as increasing requests for international cooperation and risk-assessing its non-profit sector.

Recent removals from the FATF grey list and black list

Just as countries are regularly added to the black and grey lists, countries that progress in addressing their AML/CFT deficiencies are removed. With that in mind, the FATF recently removed the following countries from the grey list.

Burkina Faso: After a four-year spell on the grey list, Burkina Faso was removed in October 2025. Announcing the decision, the FATF praised the country’s progress with measures such as strengthening the risk-based supervision of financial institutions and DNFBPs, maintaining up-to-date beneficial ownership information, implementing targeted financial sanctions regimes, and improving the ability of law enforcement agencies to combat terrorist financing.

Croatia: Croatia was added to the grey list in June 2023 amid concerns over its ability to detect and investigate terrorist financing, support non-profits vulnerable to abuse for terrorist financing purposes, and implement UN financial sanctions, among others. The FATF has now welcomed Croatia’s progress in addressing these deficiencies, and has encouraged the jurisdiction to continue its outreach efforts on terrorist financing risks to the non-profit sector.

Jamaica: In 2020, Jamaica was added to the grey list and committed to amending its customer due diligence obligations (CDD). Since then, Jamaica has worked to implement its action plan by developing a more comprehensive understanding of its ML/TF risk, including all financial institutions (FIs) and DNFBPs in the AML/CFT regime, taking measures to prevent misuse of legal entities, increasing the use of financial information, and implementing targeted financial sanctions for terrorist financing without delay. As a result of these actions, Jamaica was removed from the grey list in June 2024.

Mali: Having been grey-listed in 2021, Mali was given an action plan that included disseminating the results of its national risk assessment to relevant stakeholders, implementing a risk-based approach for supervising FIs and DNFBPs, risk-assessing its legal sector, and more. Now that it has satisfied the FATF’s requirements on this plan, Mali is no longer on the grey list.

Mozambique: In October 2025, the FATF welcomed Mozambique’s progress in remedying the AML/CFT deficiencies that had led to its grey listing in 2022. These included: ensuring cooperation among authorities in implementing AML/CFT strategies, training law enforcement agencies in gathering evidence and confiscating assets relating to financial crime, using financial intelligence to more effectively investigate cases, conducting a terrorist financing risk assessment and implementing an improved AML/CFT strategy, and providing greater resources to authorities to collect more accurate beneficial ownership information.

Nigeria: In October 2025, Nigeria also secured its removal, having spent over two years on the grey list. Among the steps it had taken were: completing a comprehensive ML/TF risk assessment and updating its national AML/CFT strategy, enhancing measures for high-risk business sectors, improving international cooperation on financial crime threats, carrying out more investigations and prosecutions of offenses, and strengthening its monitoring of non-profit organizations at risk of terrorist financing threats without disrupting legitimate activities.

Philippines: The decision to remove the Philippines from the grey list follows nearly four years of the country working closely with the FATF to address and rectify strategic deficiencies identified in its financial regulatory framework. The FATF commended the Philippines for its significant progress, particularly in enhancing legislative measures – including mandating all relevant agencies to actively participate in national risk assessments concerning ML/TF in October 2023. An on-site evaluation confirmed the effective implementation of these reforms, leading to the country’s removal from the list in February 2025.

South Africa: Added to the grey list in February 2023, by October 2025, South Africa had made enough progress to ensure its delisting. In its announcement, the FATF noted specific measures taken by the jurisdiction, such as improving the risk-based supervision of DNFBPs, ensuring authorities’ access to beneficial ownership information, and punishing violations of beneficial ownership reporting obligations, updating its terrorist financing risk assessment, and demonstrating an increase in investigations into complex ML/TF cases in line with its risk profile.

Tanzania: The FATF has welcomed Tanzania’s progress in improving risk-based supervision of FIs and DNFBPs, investigating and prosecuting financial crimes, implementing a national CFT strategy, and advancing other priorities outlined in its October 2022 action plan. The country has therefore been removed from the grey list and is no longer subject to increased monitoring.

Türkiye: In 2021, Turkey was added to the grey list and committed to implementing its FATF action plan by enhancing AML/CFT supervision, imposing strong penalties for violations, and improving the use of financial intelligence. In June 2024, Turkey was removed from the grey list due to positive improvements.

Grey list and black list screening and monitoring

Given the increased risk of ML and TF posed by blacklisted and greylisted countries, most financial authorities require firms to have appropriate risk-based AML/CFT protections to mitigate that threat.

Accordingly, firms must screen customers against the FATF black list and grey list during onboarding and throughout their business relationship, monitoring their transactions on an ongoing basis. To screen accurately, firms should ensure that their CDD measures verify their customers’ residence in, or business with, the listed countries. They should also check that their transaction monitoring software can scrutinize the size, frequency, and patterns of transactions involving high-risk countries to determine whether criminal activity, such as ML, is occurring.

When suspicious activity is detected, firms must submit suspicious activity reports (SARs) to the appropriate financial authorities to take enforcement actions.

The State of Financial Crime 2026

The State of Financial Crime 2026 report provides the granular data needed to stay informed as this year progresses, sourced from 600 global industry leaders. To stay ahead of the curve and understand the specific trends impacting your region, download the full report today.

Download nowOriginally published 23 March 2020, updated 20 February 2026

Disclaimer: This is for general information only. The information presented does not constitute legal advice. ComplyAdvantage accepts no responsibility for any information contained herein and disclaims and excludes any liability in respect of the contents or for action taken based on this information.

Copyright © 2026 IVXS UK Limited (trading as ComplyAdvantage).